AccessLine Technologies holds a very competitive position within the marketplace. They are the first company to offer the ability to manage a multitude of telecommunication channels under one single number. For this service, they’ve coined the term “One Person, One Number”. Apex Investment Partners are looking into providing financing for AccessLine. However, the terms of the deal is a challenge.

Josh Lerner

Harvard Business Review (296028-PDF-ENG)

October 27, 1995

Case questions answered:

- Valuation Revision by Apex Investment Partners.

- Proposed changes to the Rights and Preferences of Series B Preferred Stock.

Not the questions you were looking for? Submit your own questions & get answers.

Apex Investment Partners (A): April 1995 Case Answers

This case solution includes an Excel file with calculations.

Memorandum

To: Apex Investment Partners

Subject: AccessLine Technologies Investment Opportunity

Date: May 29th, 2019

Re: Proposed financing for AccessLine Technologies by Apex Investment Partners.

AccessLine Technologies holds a very competitive position within the marketplace. They are the first company to offer the ability to manage a multitude of telecommunication channels under one single number. For this service, they’ve coined the term “One Person, One Number”.

In addition to this, AccessLine is poised for rapid international growth. They have a very strong management team with experience within the industry, they’ve met or exceeded financial expectations for each of the past seven quarters, and they operate using modest capital and operating expenditures.

They’ve also developed multiple partnerships with key players in the telecommunications industry, contingent on the ability to raise the fees for their services as the use of their services increases.

AccessLine’s ability to offer such a differentiated service at a price so much lower than its competitors makes it an attractive investment. They have extraordinary potential for rapid growth, and their cash flow is projected to turn positive in the third quarter of this year.

Members of their management have successfully led companies within the same industry to a buyout in the past, and they have a good chance of going public relatively soon.

All this being said, just like any investment, there are some risks that come along with AccessLine Technologies. For starters, there is a substantial degree of uncertainty regarding AccessLine’s potential prospects in the future.

A good way to combat this risk would be to negotiate the lowest current valuation possible, which would give Apex Investment Partners a better chance of securing a positive return; however, AccessLine has made it clear they feel strongly about the company being priced at a premium.

For Apex to avoid taking on more risk than it can handle, a common ground regarding the valuation would need to be found. In addition to this, the terms of the agreement outlined by AccessLine are much less strict than the terms Apex has grown accustomed to in the past. It appears the executives at AccessLine are solely in search of capital to work with, not guidance or oversight when it comes to future business decisions.

AccessLine’s exit value would be maximized if the company made an initial public offering. Companies go public when they’re in great shape financially, and considering the fact that AccessLine is expected to continue its rapid growth in the foreseeable future, this would be the appropriate time to conduct an IPO.

It is estimated that an IPO after Apex Investment Partners’ investment would bring in proceeds of $156,333,156 at $10.50 a share (if the IPO occurred before June 30th, 1996) or proceeds of $178,666,464 at $12 per share (if the IPO was after June 30th, 1996). These potential proceeds are significantly more than what a merger or asset sale would bring to AccessLine.

Up until this point, AccessLine Technologies has financed itself by raising over $15 million in private money. They raised this money in their Series A financing round from five companies: Bella Canada, Southern New England Telephone, Ameritech, Bell Atlantic, and McCaw Cellular Communications.

They chose this strategy because it involved licensing their service to these companies instead of attempting to distribute it themselves, which allowed the “One Person, One Number” service to be brought to the market much faster.

The implication of this financing strategy is if AccessLine wishes to attain more funding to expand its operations, it cannot give the new investors better terms than the ones previously mentioned because the original investors have to approve the terms for the second round of financing.

The reason Mr. Kranzler turned to Apex Investment Partners for more funding instead of the Series A investors is that he is looking to gain capital to work with that isn’t a package deal with a strategic partnership.

The terms Accessline has proposed for the Series B financing round are not very attractive for Apex; they do not adequately address the risks of the investment.

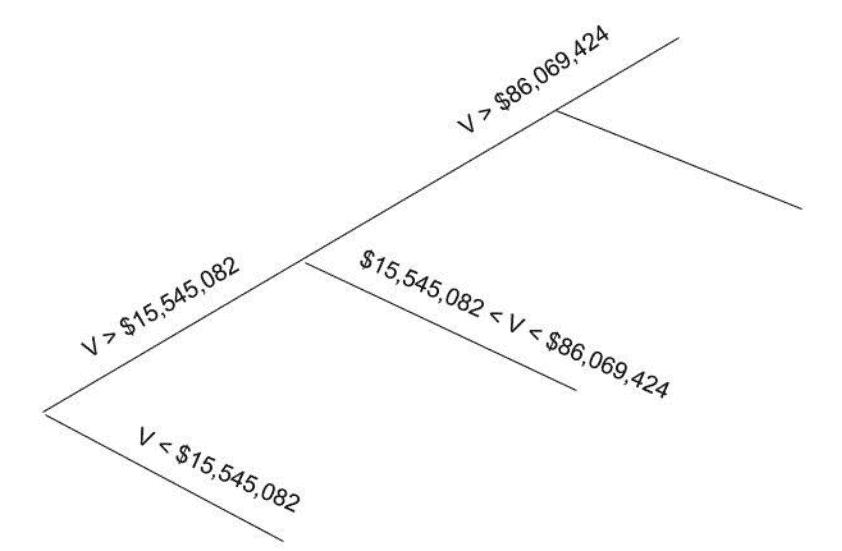

For starters, if the given terms are accepted, in the case of a buyout/IPO in which the company is valued anywhere between $31,545,082 and $119,136262, Apex Investment Partners would only receive the amount of money they put into Accessline and nothing more.

It goes without saying that not only is this a huge range, but the $119.136 million minimum price tag required for Apex to make a profit is a very steep one.

In addition to this, there are no terms in place that incentivize the executives of Accessline to pursue this $119 million mark (or punish them if they don’t reach it by a certain date). They would actually receive a larger portion of the buyout if they stay just below this number, which is obviously a conflict of interest and not beneficial to Apex Investments.

Listed below are the “waterfall” diagrams for both merger/acquisition and IPO scenarios for the proposed term sheet. All of the other term sheets we’ve examined contained clauses that either rewarded the executives at the company receiving the funding for a timely sale of the firm or punished them for each quarter that a sale didn’t occur. this term sheet contains neither.

In addition to this, the other term sheets we looked at included cumulative dividends, while the one proposed by Accessline promises noncumulative dividends. This means the executives at Accessline can choose whether or not they pay dividends to the investors and have zero incentive to sell the company sooner rather than later.

Series A Merger/Acquisition

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!