Apex Technology Co., Ltd is a printing supply and chip manufacturer situated in China. Along with a consortium of private equity firms PAG Asia Capital and Legend Capital, Apex acquires a firm, Lexmark International Inc, which is much larger than each of the three firms. This report discusses in detail the various factors of the acquisition like the purchase price, the financing structure, the participants, and possible adjustments to the financing plan.

Xiangyang Ma, Hongchuan Zhao, Tieshan Li

Harvard Business Review (W18575-PDF-ENG)

September 18, 2018

Case questions answered:

- What is the motivation for Apex Technology Co. Ltd.’s acquisition of Lexmark?

- Calculate Lexmark’s enterprise value (market multiples approach). Did Apex pay a reasonable price for the company?

- According to the case, which forms of financing will Apex use to complete the acquisition? What role does the trading scheme play in Apex’s financial plan?

- Do you think it is profitable and wise for PAG and Legend to fund Apex’s acquisition of Lexmark? Why or why not?

- Do you think Apex should adjust its financing plan? If so, how?

Not the questions you were looking for? Submit your own questions & get answers.

Apex Technology Co. Ltd.: Financing an Acquisition Case Answers

This case solution includes an Excel file with calculations.

I. Introduction – Apex Technology Co. Ltd.: Financing an Acquisition

Apex Technology Co. Ltd., a printing supplies and chips manufacturer situated in China, along with a consortium of private equity firms PAG Asia Capital and Legend Capital, acquires a firm, Lexmark International Inc., which is much larger than each of the three firms.

This case study report discusses in detail the various factors of the acquisition of Lexmark International Inc., like the purchase price, the financing structure, the participants, and possible adjustments to the financing plan.

II. The Acquisition

The motivation for this acquisition by Apex Technology Co. is to achieve its internationalization objective in 2015 of using the capital markets to become an international corporation. In other words, they are trying to achieve a global market share in a short period.

This objective is realized by acquiring a larger company like Lexmark, a company with substantial global market share and market penetration, a higher market segmentation level, and access to various patents and technology.

This acquisition can be considered a horizontal acquisition because Apex and Lexmark target the same customers. Those who buy printers would buy printing supplies as well.

For context, Apex Technology Co. is trying to acquire a company positioned as the 8th largest market share in the world (for laser printer share and ECM), distributing products across 170 countries, shipping 1,315,000 products in 2014, and having a 4.3% global ECM business that has better and improving margins than the printing business.

They also possess 2000 patents in the printing industry and are currently positioned on high-end market segmentation in the office area, allowing them to sell in premiums and make it difficult for competitors to copy the design and technology.

Another reason for this acquisition is to gain control over a multinational corporation with a growing-demand product. Lexmark has been a global manufacturer of laser printers since 2013, a product that is the future in the printing industry due to its standalone growth (4.9 %) in sales despite the downtrend in other general printing supplies (inkjet printer included).

It seems that Apex Technology Co. (or Seine) is trying to capture the growth momentum before the laser printer market matures and progresses further in sales and research with Lexmark’s existing patents.

III. Lexmark’s Enterprise Value based on Relative Valuation

Before calculating the multiples, comparable firms have to be identified. In this case, comparable firms are known by looking at Lexmark’s annual report and Top-10 Global Printing Manufacturer’s Shipment in 2014 (Ma, et al., 2018).

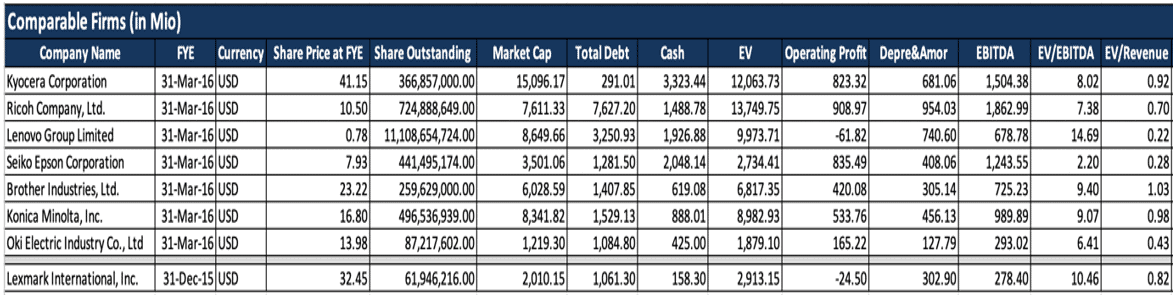

There are 7 comparable firms selected, which are Kyocera Corporation, Ricoh Company, Ltd., Lenovo Group Limited, Seiko Epson Corporation, Brother Industries, Ltd., Konica Minolta, Inc., and Oki Electric Industry Co., Ltd (Appendix 1).

Appendix 1: Comparable firms

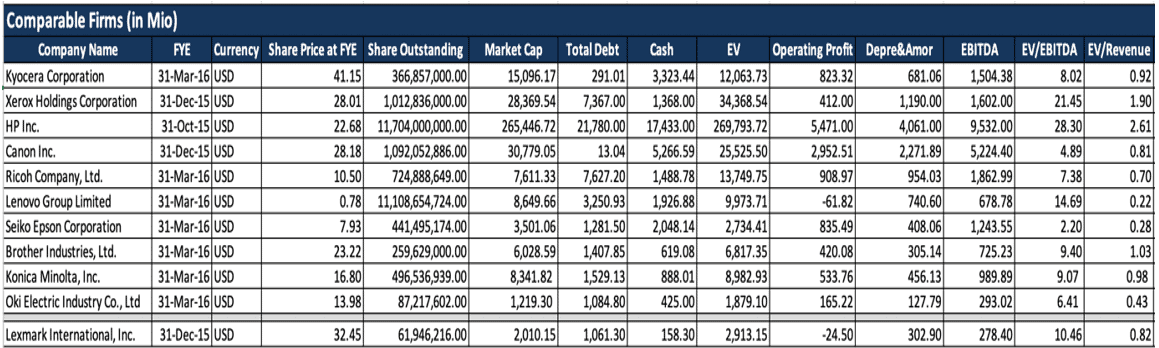

These comparable firms exclude companies that have significantly larger market capitalization compared to Lexmark (Appendix 2), such as HP Inc. and Canon Inc.

Appendix 2: Comparables excluding that have significantly larger market capitalization compared to Lexmark

By calculating comparable firms’ enterprise value and EBITDA using the following:

EV = Market Cap + Total Debt – Cash

EBITDA = Operating Profit + Depreciation and Amortization

Appendix 3 shows the EV/EBITDA multiple generated (Alert & Gill, 2016). The average EV/EBITDA of comparable firms is 8.17x, resulting in…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!