This "Arbitrage in the Government Bond Market?" case study allows students to create two synthetic bonds and determine how the price of these bonds should relate to callable bonds. It deals with the treasury market, the principles of arbitrage, and frictions in the bond markets.

Michael E. Edleson; Peter Tufano

Harvard Business Review (293093-PDF-ENG)

January 08, 1993

Case questions answered:

- Create the two synthetic bonds described in the case. How should the price of these synthetics relate to callable bonds? Why? On January 7, 1991, how much would it cost to create the synthetic using the ‘05s? The ‘00s?

- On January 7, 1991, how could Thompson exploit this apparent anomaly for investors who own the 8.25 May ’00-’05? What can investors not owning the callable bond do to profit?

- What might underlie the odd relative prices of the bonds Thompson is considering?

- Why should the treasury issue callable debt? When should they exercise their right to call or redeem the bonds? Why would corporations issue callable debt? Why should investors want to buy callable debt?

Not the questions you were looking for? Submit your own questions & get answers.

Arbitrage in the Government Bond Market? Case Answers

1. Introduction – Arbitrage in the Government Bond Market?

This paper studies the case of Samantha Thompson, who works at Mercer and Associates. In her work, she found arbitrage opportunities in the U.S. government bond market on callable debt.

To assess whether these arbitrage opportunities exist, we construct alternative portfolios with the same payoff to see if there is a case of mispricing and suggest possible trading strategies to seize the arbitrage opportunities in the market.

We then look into ways of explaining pricing differences and reasons to issue and buy this callable debt.

In the second part of this paper, we will explain some exercises to understand further the pricing of callable debt and the value of the call option.

2. Replicating the callable bonds.

Samantha Thompson has reason to believe the 8.25 May ’00-’05 bonds are overpriced. This section will set up two synthetic bonds to replicate the traded security and determine whether there are market frictions in this bond market.

The callable bond is similar to a normal bond, with the important difference that the issuer of the bond can call it. One of the reasons for calling a bond is changing interest rates.

For example, assume a callable bond issued with a 5% coupon rate and a yield of 5%. If interest rates in the market were to decrease, the issuer would call the bond and pay the principal with a new loan made at a lower interest rate.

Due to the insecurity of the buyer of the callable bond, these bonds tend to be cheaper, i.e., have higher yields than a similar non-callable bond with the same coupon and maturity. The case presented here involves a specific callable bond. The annualized coupon rate is 8.25%, the bond makes semiannual payments of $4.125 and has a face value of $100.

The bond matures on the 15th of May 2005 and can be callable as of the 15th of May 2000. To analyze whether the callable bond is over or underpriced, two synthetic bonds can be created.

Not called callable-bond:

Assuming that the bond is not called, the bond is the same as a normal bond with an 8.25% coupon that matures on the 15th of May, 2005. As there is no such bond in the market as of the 7th of January 1991, when the analysis was done, two other securities were used. The first is a non-callable bond that matures in May 2005.

For simplicity, we assume that the bond matured on the 15th of May 2005. It has a coupon of 12%. The second security is a Treasury STRIPS that matures in May 2005 again. For simplicity reasons, we assume that the maturity date is the 15th of May 2005.

The STRIPS is like a zero-coupon bond that pays the par value at maturity. To compare the synthetic bond portfolio and the callable bond, one needs to make sure that they yield the same pay-off.

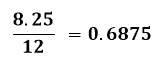

The coupon payments, hence the amount invested in the non-callable treasury bond, can be calculated as follows:

As the coupon payment of the treasury bond (12%) is higher than the coupon payments of the bond that is to be replicated (8.25%), only a fraction of the treasury bond is bought.

Accordingly, in this case, it is assumed that fractional quantities of securities can be traded without further limitations.

This means that for every callable bond, one should…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!