The Blue Heron Capital Partners case study deals with a socially-responsible hedge fund. Two firms, AstraZeneca plc and Medco Health Solutions, Inc., both practicing social responsibility, have options valued written on them.

Kathleen Hevert

Harvard Business Review (BAB711-PDF-ENG)

February 01, 2012

Case questions answered:

- What is distinctive about option security? Can calls and puts be valued using the traditional discounted cash flow model (DCF) model? Why or why not?

- Consider the Medco call option with a $40 exercise price and an October expiration. Using the riskless hedge approach and monthly binomial trials, what is this option worth today?

- Now consider the Medco call option with an exercise price of $40 and a January expiration. Using the riskless hedge approach and monthly binomial trials, what is the option worth today? How do you explain the difference between values for the October and January calls?

- What is the value of the Medco call option with a $40 exercise price and an October expiration using the Black Scholes option pricing model? Why does this value differ from the value using the binomial approach?

- Let us now turn to the AstraZeneca call option with a $40 exercise price and an October expiration. Using the riskless hedge binomial approach and the Black Sholes option pricing model, what is this option worth? For now, disregard the dividend AZN is expected to pay in September. How does this value compare to the MHS call with the same contract terms? What accounts for the difference?

- Returning to the AstraZeneca call option with a $40 exercise price and an October expiration, how do you expect the September dividend to affect the valuation? Why? Use the Black Sholes option pricing model to validate your prediction. Assume that the 2008 dividend amount and timing will be identical to that of 2007. Are there any problems using the Black-Scholes model to value an option on a dividend-paying stock?

Not the questions you were looking for? Submit your own questions & get answers.

Blue Heron Capital Partners Case Answers

This case solution includes an Excel file with calculations.

1. What is distinctive about option security? Can calls and puts be valued using the traditional discounted cash flow model (DCF) model? Why or why not?

An option is a right, usually obtained for a fee, to buy or sell an asset within a specified time at a set price, which comes in many forms, not only as stand-alone contracts but also as an embedded element in securities (such as convertible bonds) and investments in real assets.

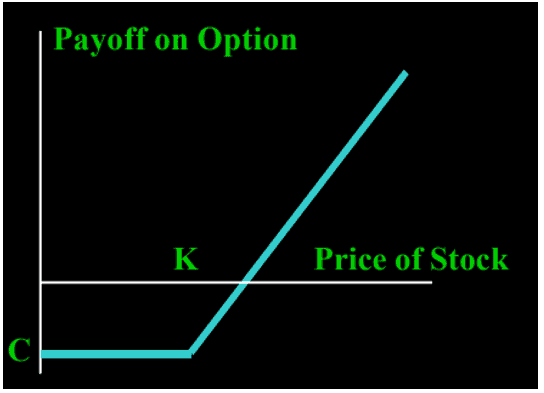

The payoff on the option diagram presented in Exhibit 01 can be used to illustrate the distinctive character of an option.

This diagram shows that the value of an option increases as the value of stock increases, and the limited losses and unlimited upside are faced by the option holder.

Basically, the risk-adjusted discount rate for the underlying asset can only be used to evaluate derivatives of that asset if the derivative has the same risk as the underlying asset.

Options are riskier because they are leveraged claims. Even small fluctuations in the value of the underlying asset can greatly affect the return on a small option investment (option premium).

Also, the holder may lose 100% of his investment in the call option, while the holder of the underlying asset almost never loses 100% of his investment.

For an option, the beneficial change in the value of the asset is limited, but for the underlying asset itself, the beneficial outcome is infinite.

These factors, combined with the fact that the risk profile of an option changes every time the value of the underlying asset changes, make estimating the appropriate risk-adjusted discount rate an impossible task. Therefore, we cannot use DCF to assign options.

Exhibit-01

2. Consider the Medco call option with a $40 exercise price and an October expiration. Using the riskless hedge approach and monthly binomial trials, what is this option worth today? In order to build the binomial tree, you need to estimate the volatility for Medco. Using the stock prices provided in the Excel file, follow these steps:

a. Compute daily return for each trading day using adjusted prices as follows:

![]()

b. Find the standard deviation of daily returns over the past year.

c. To annualize the standard deviation, take the standard deviation of daily return and multiply by the square root of 260 (the approximate number of trading days in one year).

For the year ended July 18, 2008, the daily volatility of MHS was approximately…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!