This "Carter International" case study deals with the acquisition of Hope Enterprises by Carter International, a hotel company. It discusses the factors taken into consideration in identifying whether Hope Enterprises was a worthy company to invest in.

Michael J. Schill

Harvard Business Review (UV7275-PDF-ENG)

December 21, 2016

Case questions answered:

- Overview of the business – Carter International.

- Statement of Problems

- Analysis

- Recommendations

Not the questions you were looking for? Submit your own questions & get answers.

Carter International Case Answers

This case solution includes an Excel file with calculations.

Overview of the Business – Carter International

Carter International is an established casino business looking to acquire Hope Enterprises, which targets a market that has yet to be tapped. The former oversees 79,000 rooms with both its flagship hotels and international presence.

The current management at Carter sees the gaming industry as a growing industry and wants to expand into the mid-market gamblers that Hope currently attains. Analysts have suggested that Hope partner with a larger hotel company to continue successful operations.

Hope is in high demand due to the location of its casinos, which investors see as a very sought-after company. With Carter International acquiring Hope, both sides would benefit as Hope would expand Carter into an untapped market, and Carter would provide value-adding opportunities to Hope.

Statement of Problems

Carter International is considering acquiring Hope Enterprises. Before its decision, it must determine if Hope is an excellent strategic fit as well as the rate of return required by Carter. Using the seven-year forecasts, it must be determined if Hope’s current share price of $15 is an abnormal buying opportunity.

Also, Carter must forecast utilizing synergies of the potential merger to determine what offer to bid for Hope, along with using the multiples approach to see the implied share price of comparable companies. Finally, Carter International must re-evaluate its capital structure mix to determine how to finance Hope.

Analysis

The first part of this analysis was finding Carter International’s required rate of return. A multitude of variables first had to be assumed, such as the 40% tax rate given in the case, cost of debt of 6.90% from the bond rating of a B grade, market risk premium of 5% from exhibit five, price per share of stock as $15 from the case, 65 million shares outstanding given in the case, a beta of 1.45 from exhibit 2B, and a risk-free rate of 2.75% as provided in exhibit five as the thirty-year US government bond yield.

The thirty-year rate was used due to the five-year rate being too short of a time projection. The book value of debt of $702.90 was found from Hope’s long-term debt and the current portion of debt due, and market equity was found by utilizing Hope’s price per share and shares outstanding.

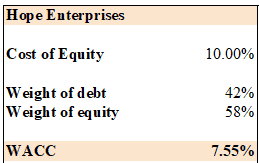

Total capital was found from the market value of equity and the book value of debt. From there, the cost of equity was found to be 10.00% using CAPM. The weight of debt was found to be 42%, while the weight of equity was 58%. From all these variables, a WACC for Hope Enterprises was found to be 7.55%.

The DCF for the stand-alone basis was then found. Revenue was assumed to…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!