This report will look at the methods to incorporate the ESG factor into the investment strategy, the different dimensions of the ESG and its effects, the challenges of accounting for ESG in valuations, and the implications of ESG in valuation. Specifically, this case study discusses the Environmental, Social, and Governance factors that affect the valuation of the CLP Group.

Entela Benz and Ellen Orr

Harvard Business Review (ST52A-PDF-ENG)

May 06, 2018

Case questions answered:

- What are the possible ways to project ESG KPIs into financial drivers? How should analysts incorporate ESG factors into company share valuation models?

- Are ESG factors reflected in the base case valuation? If not, why?

- Which ESG KPIs have the biggest impact on utility companies’ valuation?

- Are all three dimensions equally important (social and governance)? Is this industry-specific?

- Should any adjustments be made to given valuations? For example, should the WACC only be adjusted, or should growth be as well?

- Can you identify any shortfalls of ESG valuation? Are these specific to CLP Group, to the utility industry, or are they general shortfalls applying to any valuation? Please specify

- If you were an equity analyst, what would your recommendation be on CLP shares?

- Do you agree or disagree with Susan’s viewpoint that integrating ESG factors in company valuations will be increasingly important?

- Are there any other key questions you think should be asked and answered?

Not the questions you were looking for? Submit your own questions & get answers.

CLP Group: Environmental, Social and Governance Factors and Their Effects on Valuation (A) Case Answers

This case solution includes an Excel file with calculations.

1.0 Introduction – CLP Group: Environmental, Social, and Governance Factors and Their Effects on Valuation (A)

This case study discusses the Environmental, Social, and Governance factors that affect the valuation of the CLP Group.

Investors have been increasingly incorporating the Environmental, Social, and Governance (ESG) factors into their investment strategy over the years. This phenomenon is caused by the belief that companies that strive to adhere to ESG rules would outperform companies that do not.

This is based on the theory that high-scoring ESG companies would have more customer support, would be better at reducing costs, and would have lower tail risk, leading to a higher valuation.

However, currently, there exists no consensus ESG integration method for valuation. Analysts would use their own integration methods, be it arbitrary or quantitative, to value companies.

This would lead to the market participants being unclear about the effects of the ESG factor on equities. Hence, some would believe that mispricing due to ESG factoring exists, which brings about investment opportunities.

This report will look at the methods to incorporate the ESG factor into the investment strategy, the different dimensions of the ESG and its effects, the challenges of accounting for ESG in valuations, and the implications of ESG in valuation.

2.0 ESG Strategy Dimensions Effects

A company that adheres to ESG is a company that cares for the environment, social and labor rights, and its corporate governance while also prioritizing business profits and returns for shareholders.

The implementation of each dimension (environment, social, and governance) would often have different costs and benefits to a firm, depending on firm characteristics like industry, geography, business, etc.

This report mainly focuses on the company CLP Power Company Hong Kong Limited (CLP) and the effects of ESG on it. Thus, the firm characteristics are the utilities sector, operating in Hong Kong, and the business of generating, transmitting, and retailing electricity.

The environmental dimension would require companies to refrain from utilizing non-renewable resources and activities that would cause harm to the environment.

For a utility company like CLP Group, this would look like building/purchasing renewable energy plants, R&D to develop the technology to reduce emissions, or gaining this technology through acquisitions. As the utility sector is a capital-intensive sector, these costs would be high, typically in the form of capex and fixed costs.

For the benefits, researchers have found that customers are willing to pay or purchase more from companies that are actively addressing environmental issues (Mckinsey, 2020).

Similarly, acquirers are willing to pay a higher premium to acquire these ESG-abiding companies. While this means that CLP’s revenue could increase, the SCA in Hong Kong caps the return of electric utility firms in the country at 10-11%, meaning that CLP Group is not able to increase its service price. Hence, the environmental dimension benefits are limited in terms of sales growth.

A firm that addresses social and labor issues could see higher wages and increased spending on supply chain safety standards (Bos, 2014). It could also see more spending on fees for audits, site checks, and employee training.

All these costs could apply to the Group as it has many energy plants and is vertically integrated. Multiple research papers stated that such investments could increase employee satisfaction and thus increase work productivity.

For CLP Group, this could mean less time and resources to run operations and achieve objectives. Hence, the benefit would be sustainable reductions in costs for long-term value.

Moving on, a company that upholds governance would have independent auditors and compensation committees, as well as manage risks responsibly and provide transparent, high-quality reporting. This would lower the likelihood of the CLP Group being engaged in misconduct and the likelihood of sudden large losses.

Hence, the benefit for CLP is the perception of lower risk by investors and regulators towards the firm, reducing the cost of capital and easing the process of securing financing (Polbennikov et al., 2016).

In short, for the CLP Group and the utility sector in HK, the environmental dimension only improves image with much costs incurred, the social dimension results in a net gradual decrease in cost margins over time, and the governance dimension reduces the cost of capital with less cost.

3.0 ESG Incorporation in Valuation

ESG KPIs are good measures to assess the ESG performance of a company and to target the specific affected areas of a company, like sales growth, profit margins, and cost of capital. Analysts can use ESG KPIs and/or ESG scores to determine the impact of the ESG factor on these areas during valuation.

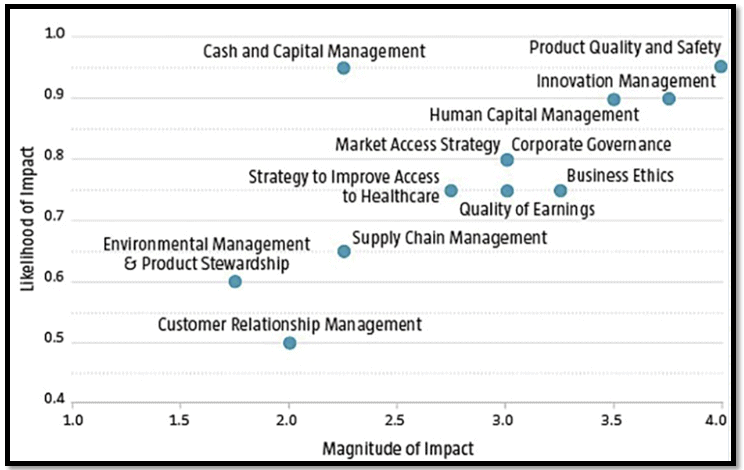

For ESG KPIs, since there are numerous KPIs available, the KPIs with the highest impact on financial performance and the highest likelihood of impact are usually selected to be used in valuation to avoid over-complexing the model. One way to determine such KPIs is to assess the KPI’s strength of linkage to CLP Group’s valuation metrics and core business drivers using a Likert scale (strong, moderate, weak) and then plot the materiality matrix.

The inputs could be done subjectively by the analysts, but inputs backed by primary research (survey) and statistics (regression test) would be preferred. Analysts can conduct the survey on executives of utility companies in HK or run a regression using a financial metric like revenue as the dependent variable and KPI numbers as the predictors, finally selecting the KPIs that are statistically significant.

As such, Appendix 1 shows the general materiality matrix for all industries, whose inputs are obtained through a combination of analysts and surveys. Research also found specific key materiality issues for the utility industry, namely climate strategy, releases & emissions, and ecological footprint (Schramade, 2016).

Appendix 1: Average Materiality Matrix Across All Industries (RobecoSam, 2020)

The analysis decided that the materiality issues key to CLP Group are…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!