Continental Carriers, Inc. (CCI) is a U.S. trucking company that is looking into getting a loan for the purchase of another company. Since the company directors have conflicting stands on taking on a debt, it was hard for CCI to come up with a decision.

W. Carl Kester

Harvard Business Review (291080-PDF-ENG)

June 25, 1991

Case questions answered:

- Considering Continental Carriers, Inc.’s capital structure, and given the nature of the business, how much debt can it support?

i. Evaluate the question from the interest coverage ratio perspective,. - Consider the EBIT chart. What information can you extract from it?

- Which Financing alternative is best for shareholders? Consider the impact of each, in turn, on the following:

i. EPS level

ii. EPS growth

iii. EPS Volatility.

iv. Capacity to pay dividends - Why not assume a lot of debt?

i. Risk

ii. Return - Does the sale of new shares pose any risks or potential problems?

i. In what sense, if any, will the sale of new shares “dilute” the stock of existing shareholders? - What do you recommend Continental Carriers, Inc. to do?

Not the questions you were looking for? Submit your own questions & get answers.

Continental Carriers, Inc. Case Answers

This case solution includes an Excel file with calculations.

CONTINENTAL CARRIERS, INC. (CCI)

MIDLAND ACQUISITION EXECUTIVE SUMMARY

Overview of the Company – Continental Carriers, Inc. (CCI)

Continental Carriers, Inc. (CCI) is a motor carrier founded in 1952. In 1982, CCI went public. In 1988, it planned to buy Midland Freight, Inc in a $50M cash takeover. Midland Freight, Inc will bring to CCI $8.4M in EBIT per year.

CCI’s policy of stable dividends and avoiding long-term debt (stock offering or short-term bank loans).

How to Finance Midland Acquisition?

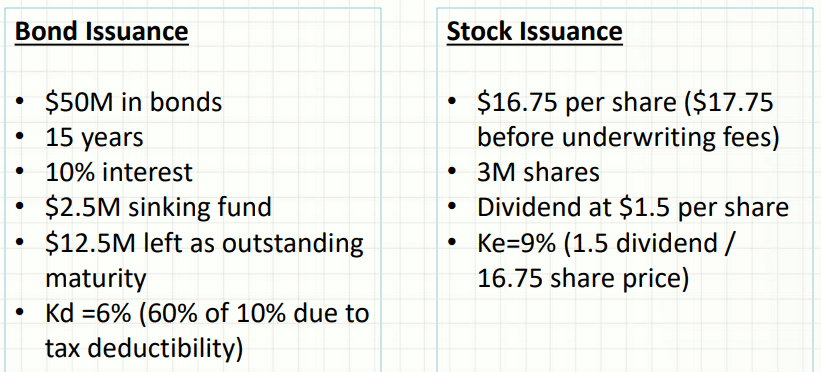

Financing $50M…

(CFO Assumptions/Options)

Directors’ Challenges & Analysis

Director 1 – PRO-EQUITY

- Cost of debt at 8% (the sinking fund is missing)

- Stock issuance has a smaller cost than bonds

- Bond added risk to Continental Carriers, Inc. causing stock volatility

Director 2 – PRO-DEBT

- Against stock issuance, because the acquisition would net $5M (or 10%)

- Additional dividend of $4.5M is required

Director 3 – PRO-DEBT

- $17.75 per share is a “steal”

- Book value of the company is $45 per share in 1987

- Dilution of management voting rights

Director 4 and 5 – PRO-DEBT

- Post-acquisition earning of $34M (before interest and taxes = EBIT)

- Dilution of EPS to $2.72 if common stocks are sold

- EPS up to $3.87 if only debt is used

Director 6 – MIXED/OTHER

- Continental Carriers, Inc. has no long-term debt, while EPS is the lowest in the industry

- Preferred stock (not to be taken into account)

How Much Debt can CCI Support?

Interest Coverage with $50m New Bond is…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!