The CFO of County Line Markets, Ron Winston, had the idea of using a real options approach (ROA) to determine when and if the store should be converted to a superstore. The report considers various binomial lattice models to conclude whether or not to begin the expansion of a superstore, depending on certain variables.

Tom J. Cook, Lou D'Antonio, Ron Rizzuto

Harvard Business Review (NA0351-PDF-ENG)

May 01, 2015

Case questions answered:

- Summarize the limitations of NPV analysis in this situation. What is wrong with traditional NPV analysis augmented with risk analysis?

- Determine what options are embedded in CLM’s investment Decision.

- Estimate the volatility of the present value of future free cash flows for the real options analysis using the Arzac [1] range-based estimate.

- Discuss the strengths and weaknesses of this method for estimating volatility.

- Estimate the volatility of the present value of future free cash flows for the real options analysis using the simulation method.

- Compare and contrast the two estimates of volatility (the Arzac and Simulation Approaches), as well as discuss the strengths and weaknesses of each method of estimating volatility.

- Construct a binomial lattice model of CLM’s real option to determine when County Line Markets should construct the superstore, assuming no entry by Walmart. Use the Copeland and Antikarov and Mun approach. Discuss the results relative to the traditional capital budgeting approach.

- Construct a binomial lattice model of CLM’s real option to determine the real option value of the project assuming entry by Walmart during the next five years–use Simulation and the Convenience Yield approaches.

- Construct a binomial lattice model of CLM’s real option, using the Azarc approach, to determine when CLM should construct the superstore, assuming no entry by Walmart.

- This case illustrates the use of real options analysis as an ‘’analytical tool.” What are the strengths and weaknesses of this approach?

- Discuss other ways that CLM could engage in “real options thinking” without going into detailed numerical calculations, such as those necessary for the binomial lattice model.

- Should CLM invest now or defer the decision to invest until a later period?

Not the questions you were looking for? Submit your own questions & get answers.

County Line Markets: Real Options and Store Expansions Case Answers

This case solution includes an Excel file with calculations.

Abstract – County Line Markets: Real Options and Store Expansions

County Line Markets (CLM, or “the Company”) needs to consider expanding one of its existing sixty-seven Indiana-based stores to form a superstore.

The main capital investment trade-off decision facing CLM is whether to replace its current store with an upgraded, more massive superstore or instead wait to receive additional information in the future that would provide insight into the overall net present value (NPV) of the project.

The CFO of CLM, Ron Winston, had the idea of using a real options approach (ROA) to determine when and if the store should be converted into a superstore. The report considers various binomial lattice models to conclude whether or not to begin the expansion of a superstore, depending on certain variables.

To construct the analyses, a discounted cash flow model was built to determine both the NPV of continuing business as usual and upgrading to a superstore, at $4.99 million and $10.61 million, respectively.

From there, volatility is estimated through two different methodologies, the Arzac method and the Copeland and Antikarov method, providing various options as to how to proceed with the valuation.

Lastly, three binomial lattice models are explained, each different depending on whether or not CLM’s competitor Walmart entered the market and using the various estimates of volatility.

In the end, it is determined that CLM should wait to invest in converting their store to a superstore and observe the future market conditions carefully.

Background – Information on County Line Markets

County Line Markets (CLM), a family-owned grocery store chain, belongs to the retail grocery industry. It occupied a significant portion of the United States. It was founded in 1905 in Indianapolis, Indiana, by Michael Lloyd, the great-grandfather of CLM’s CEO William Lloyd, and his wife, Mildred.

Beginning with only one store, Michael and Mildred built their grocery store chain to 5 stores in just ten years. With the continued growth of CLM, their son Marcus Lloyd served as the president of the CLM, and Michael became the chairman of the board. At the time when Michael handed over the reins to his son Marcus, CLM operated 15 stores in the greater Indianapolis area.

In 1980, the time Marcus retired, CLM operated 47 stores in the greater Indianapolis area, as well as eight stores located in Fort Wayne and Bloomington.

Marcus’ son Harry managed the CLM business from 1980 to 2002, a period when CLM experienced remarkable growth in competition.

However, CLM still kept a substantial growth increase in its market share during this period since CLM possessed competitive pricing policies as well as customer loyalty programs, modern stores, and organizational efficiency. CLM also expanded its product line by adding bakery, grocery, floral, and seafood departments to its stores.

In 2002, William Lloyd, the son of Harry, started managing CLM, and the growth of CLM kept taking place. By the time in 2011, it had 67 retail stores, three manufacturing operations, as well as two warehouses, and 6,750 employees, who were organized into seven departmental units, including finance, store operations, manufacturing, marketing, purchasing, human resources, and legal.

Information on the industry

In the United States, the retail grocery industry played an essential role in several industries. It was one of the largest industries in the United States.

As the data of 2011 showed, the retail grocery industry, with 3.4 million people employed, had total retail supermarket sales of $584.4 billion. More than 36,000 supermarkets were earning at least $2 million in annual sales.

On average, the American people would go more than two times a week to supermarkets, meaning that a supermarket is an essential place for Americans to live.

According to industry data, Americans would spend 5.5% of disposable income on food consumed at home, which could be bought in supermarkets, and would pay 3.9% of disposable income on food consumed away from home, such as in restaurants.

However, the percentage of household spending on food consumed at home in disposable income had declined steadily and remarkably over the past 40 years, according to Figure 1 presented in the case.

The reason for that would primarily be a result of stiff competition among retailers as well as some competition coming from outside the industry, such as restaurants serving dual-income families, thus fueling a steady growth in “food consumed away from home.”

These increasingly competitive factors caused the profit margins in the retail grocery industry to vary remarkably over the past three decades. For instance, the before-tax margins can be as low as 1.11% in 1988/1989 and can be as high as 2.80% in 2007/2008.

Information on the problem in the case

The CEO of County Line Markets, William Bill Lloyd, the CFO of CLM, Ron Winston, and the vice president of operations, Jerry Williams, would have a debate on the issue of whether to consider the expansion investment’s value by adopting the real options analysis or by applying the NPV method.

Ron Winston, the CFO of CLM, was trying to convince the CEO to use real options analysis when evaluating the investment.

While Jerry Williams, the vice president of operations, had been skeptical of real options. Note that both the real options method and the NPV method are based on many assumptions, meaning that the results coming from either method would not always be 100% correct compared to the real-world consequences.

We will present later on in the report the pros and cons of the real options analysis, as well as the NPV method.

Analysis

a.) DCF

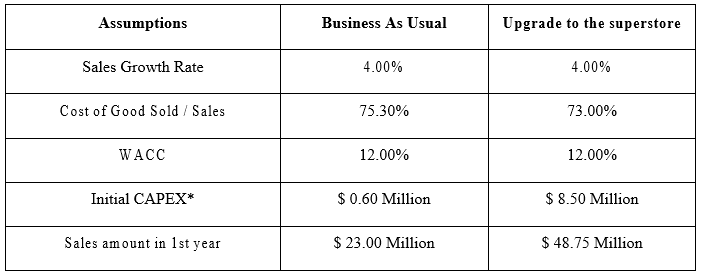

The main assumptions and results of the NPV project for Metro 1 calculated by County Line Markets through DCF are as follows.

Key Assumptions to Calculate NPV through DCF

*Capex amount = Leasehold improvements + Equipment costs

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!