In late 2006, Culinarian Cookware and its top executives were looking into price promotions for their cookware products. The senior executives were of two different views. Donald Janus, VP of Marketing, thought that such promotions were not needed as it might result in distortion of brand image, and may encourage hoarding. On the other hand, Victoria Brown, Senior Sales Manager, thinks that such promotion will expand consumers' brand awareness and bring in new customers. What strategy should the company pursue to increase sales goals?

John A. Quelch and Heather Beckham

Harvard Business Review (4057-PDF-ENG)

September 22, 2009

Case questions answered:

- Outline three reasons why Culinarian Cookware should run price promotions.

- In what ways can Culinarian maximize sales of slow movers and popular items?

Not the questions you were looking for? Submit your own questions & get answers.

Culinarian Cookware: Pondering Price Promotion Case Answers

This case solution includes an Excel file with calculations.

1. Outline 3 reasons why Culinarian Cookware should run price promotion.

Culinarian Cookware 2004 Sales and Analysis of first-time price promotion on overall revenue:

- First-time price discount of 20% for April 1 to May 31, 2004

- To pass the 20% price discount to customers, traders’ margin was reduced from 52% to 48%. Still, due to the low prices and early intimation, many traders differ the prices and pass only 10% to customers. (ignoring this for calculation)

- Discounts were made available only on CXI, which is a low-price product for Culinarian Cookware.

- Units of CXI sold during that promotion period= 184987

- Promotion Significance: 80% of purchases were from existing customers as new units, 20% were new customers

- No new advertisement other than a regular one was made for the price promotion exercise

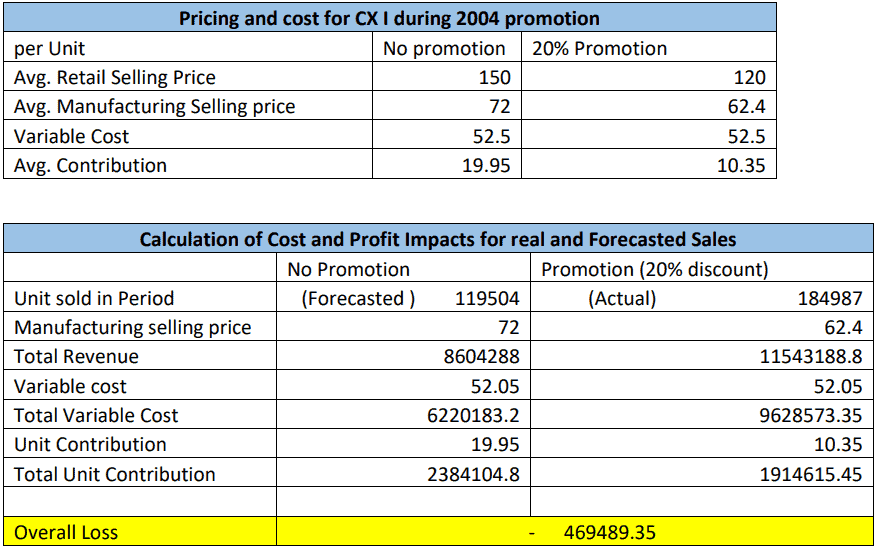

- Average sales without promotion as estimated by consultant=119504

a. Calculation of Profit impact (Total Unit Contribution) as per consultant’s View

Launching promotion activity for April and May leads to an overall decrease in profit impact. There can be many reasons for that, such as no new customers buying the CXI, traders not passing the discounts to end customers, overstocking of goods by traders to sell later, etc.

b. Calculation of Profit impact (Total Unit Contribution) as per Victoria Brown’s View

But Culinarian Cookware Senior Sales Manager Victoria Brown believed that the estimations and considerations taken by the Consultant were flawed for the following reasons:

- She believed the normal sales figures were too high. Brown reviewed sale order data for the CX1 product line (Exhibit 7) and discovered that March-May orders for 2003 — the prior year — totaled 78,778 units. She further noted that XI sales orders in the first two months of 2004 were 24% below the first two months of 2003. Therefore, she felt the most accurate method to forecast 2004 March-May “normal” sales was to set them 24% below the 2003 sales for that same time period. By Brown’s calculation, “normal” sales during the promotion period would thus have been only 59,871 units.

- Brown did not agree with the overhead cost allocations that had been added to the variable cost estimates. She felt that variable cost estimates should include only labor and raw materials, which totaled $38.64 per unit.

- Brown believed there was no reliable way to calculate cannibalization costs and inventory savings and should, therefore, be left out of the analysis.

Culinarian Cookware’s normal Sales, according to Brown’s calculation: 59871 Units

Variable Cost is equal to…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!