Destin Brass Products Co. is engaged in manufacturing brass valves, pumps, and flow controllers. The company management is facing the question of whether cost accounting and cost allocations affect competitive pricing and causes different results.

William J. Bruns Jr.

Harvard Business Review (190089-PDF-ENG)

December 04, 1989

Case questions answered:

- Use the overhead cost activity analysis in Exhibit 5 and other data on manufacturing costs to estimate product costs for valves, pumps, and flow controllers.

- Compare the estimated costs you calculate to existing standard costs (Exhibit 3) and revised unit costs (Exhibit 4). What causes different product costing methods to produce different results?

- What are the strategic implications of your analysis? What actions would you recommend to the managers at Destin Brass Products Co?

- Assume that interest on a new basis for cost accounting at Destin Brass Products remains high. In the following month, quantities produced were sold, and activities and costs were all standards. How much higher or lower would the new income reported under the activity-transaction-based system be than the new income that will be reported under the present, more traditional system? Why?

Not the questions you were looking for? Submit your own questions & get answers.

Destin Brass Products Co. Case Answers

This case solution includes an Excel file with calculations.

Please scroll down to the bottom of this post to download the additional Excel spreadsheet!

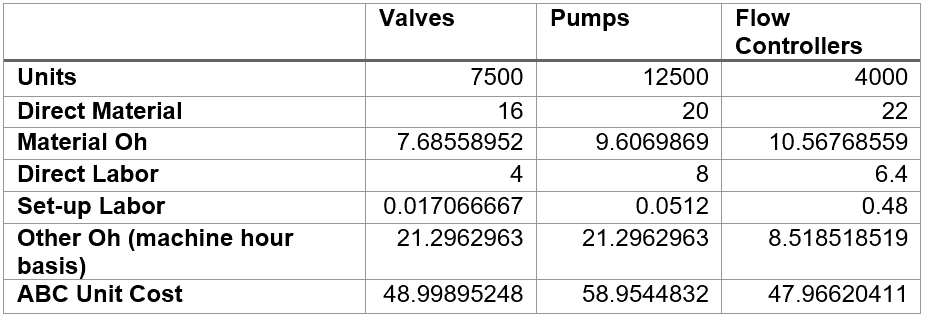

Q1: Estimate product Costs by different methods

Standard Costing

Revised-ABC

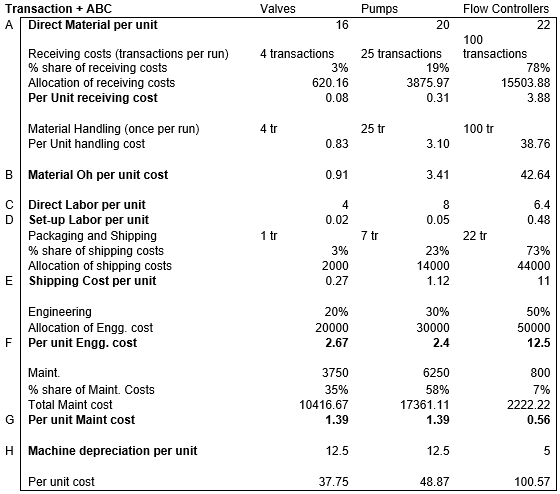

Transactional ABC – Gives appropriate weightage to split activity costs to each product line. For instance, the flow controller requires 10 components; each component is handled once per run, and there are 10 runs. Therefore, 100 transactions; hence (100 / 129) % weightage of total costs.

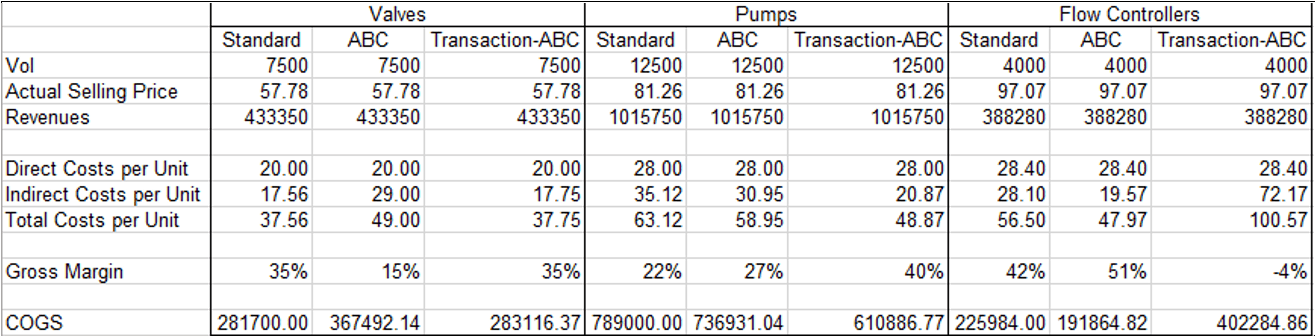

Q2. Compare cost systems

Various cost systems imply different methods of allocating overhead costs to the product line, hence different implications for product line profitability.

In the third method, Flow controllers take higher per-unit costs because of the high transaction % involved in receiving and material handling. The material handling & receiving costs are 220,000, which is 35% of direct costs, with a much-skewed distribution across product lines, thus completely changing the picture of product line profitability.

Q3. Strategic implications?

The Pumps line is much more profitable than earlier thought. So Destin Brass can further lower the prices to take on the completion head-on. In fact, they can lower their gross margin further by 5%, charge $75.18, and still reap the profit margin of the desired 35%.

The reason was that they could increase the prices of flow controllers, and still, the market was OK with it. This is a testimony that the costing system is indeed flawed. Because they are selling flow controllers at a negative gross margin under the transaction-ABC costing system. So virtually, they have no competition so far.

The market has the potential to buy at more prices. Flow controllers should be priced higher to reap a 35% margin. A price of $135 would be ideal.

Q4. Profit implications?

Cost accounting is an Internet decision. It is just a method of distributing the net COGS to individual product lines. Generally speaking, the net income shouldn’t be affected by the methods of allocation one chooses. This is proven below:

Additional File:

Excel Spreadsheet. Download here.

Did this solution help you?

(18 votes, average: 4.72 out of 5)

(18 votes, average: 4.72 out of 5)