This case study focuses on the move of Reynolds Metals on making an initial public offering of Eskimo Pie Corp.'s shares. Reynolds Metals is selling its holdings o Eskimo Pie. Despite receiving an offer from Nestle for the latter to buy the said shares, Reynolds Metals still made the IPO.

Richard S. Ruback and Dean Mihas

Harvard Business Review (293084-PDF-ENG)

November 24, 1992

Case questions answered:

- Prepare an Executive Summary for the Eskimo Pie Corp. case study.

- Discuss the company’s situation and provide an analysis.

- What are your recommendations?

- Also, prepare a financial valuation.

Not the questions you were looking for? Submit your own questions & get answers.

Eskimo Pie Corp. Case Answers

This case solution includes an Excel file with calculations.

1. Prepare an Executive Summary for the Eskimo Pie Corp. case study.

Eskimo Pie Corp. constituted a subsidiary of Reynold Metals, the makers of Aluminum Foil and other aluminum products, contributing roughly 1% of their total revenues.

The company was one of the pioneers of the frozen novelty industry, with several products well-accepted in the market, including the first and most popular chocolate-covered bar of vanilla ice cream.

Although the company was the third leading frozen novelty brand (5.3% unit share) in a highly fragmented industry, Reynolds was considering divesting Eskimo Pie’s holding, given its focus on the aluminum and packaging business.

Reynolds appointed Goldman Sachs to advise with the holding’s sale. They estimated that Eskimo Pie’s worth in 1991 would be an equivalent of 1.2 times 1990 sales or about $57 million, while Nestle Foods positioned itself as the highest of six bidders for an acquisition value of $61 million.

Eskimo Pie Corp.’s president, Mr. David Clark, has conflicting views of this acquisition by Nestle because the likelihood of centralizing the management from the current headquarters to Nestle’s strategic teams was imminent. His idea was to team up with a local investment banking firm, Wheat First Securities (Wheat First), to attempt a private Leverage Buyout (LBO). It would allow Reynolds to get liquidity from the sale while saving a local company and local jobs for Richmond residents.

Besides the licensing business line for manufacturing, distribution, and sale of Eskimo Pie brand products, they had Welch’s and Health brand products business lines, which were in the business of ingredients and packaging for the dairy industry.

The company dedicated a considerable amount of its capital budget to research and development of new products, and they were successful with ten products introduced since 1987 and actively marketed and sold in 1991.

Their not-so-conventional licensing approach consisted of charging the license contribution to the price paid for ingredients and packaging supplied to its national licensee network. It was precisely this licensing approach that reframed interested buyers from offering competitive bids.

2. Discuss the company’s situation and provide an analysis.

This case study’s main point of discussion is providing the appropriate valuation of Eskimo Pie Corp. to fund the business sale through an Initial Public Offering (IPO) compared to Nestle’s offer sale price.

Initially, Clark and Wheat First managed to raise $20 million in credit and $15 million in equity, but the offer was denied due to higher bids and the unpopularity of high-yield debt-financed LBOs. However, during the course of 1991, actual net income and total sales were considerably higher than the expected values, and Eskimo also accumulated a $13 million cash reserve.

This allowed Wheat First to work on an updated and more promising forecast. Wheat First proposed a two-step transaction. The first step consists of paying out a $4.52 per share special dividend funded on its great majority by the accumulated cash reserve. Then, it shall proceed with an IPO with a “Green Shoe” clause that will be used to pay off the remaining special dividend debt and working capital requirements.

Under both offering prices of $14 and $16, Reynolds will be able to receive an equal or larger total sale price compared to Nestle’s offer. Nevertheless, Wheat First proposal would be conditioned on the likelihood of the continuance of the new issues market’s good run compared to cash secured upfront if they decided to continue the sale to Nestle.

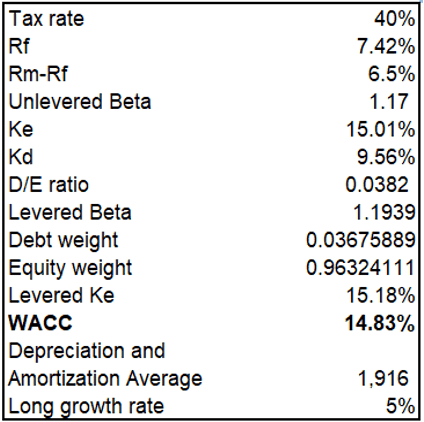

The first stage of this case valuation is focused on calculating the appropriate discount rate to use for Eskimo Pie Corp.’s valuation using the Discounted Cash Flow model. First of all, from the Comparable Companies information, we can get a reference for Eskimo’s appropriate beta level. Still, the given betas need to be adjusted for differences in capital structure by calculating the unlevered betas.

I decided to stick with the resulting average beta of 1.17. I determined a risk-free rate of 7.42%, equivalent to the ten-year treasury yield, and a conservative mark risk premium of 6.5%, given that the case does not give historical market returns and company returns to calculate through regression analysis.

For the cost of debt, I decided to use the BBB long-term bond yield, given the company’s current financial position. In order to calculate Eskimo Pie Corp.’s levered beta, we used the 1990 capital structure and an average tax rate of 40% from Exhibit 6.

By using these inputs, we found that Eskimo Pie Corp.’s levered cost of equity is 15.18%, which leads to a weighted average cost of capital (WACC) of 14.83% used for discounting their future cash flows.

Given the discrepancies in expected cash flows used by Goldman and Sachs valuation and the actual cash flows for 1991 used by Wheat First valuation, I decided to do a comparative analysis to verify how fluctuating the differences are using the DCF model under two different approaches.

From one side, I calculated the terminal value following the Gordon Growth model, determining a long-term growth rate. Subsequently, I derived Eskimo Pie Corp.’s share price…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!