The owner of Habitual Chocolate, a small, chocolate manufacturing and retailing company in London, Ontario, was looking into expanding into Southwestern Ontario. While the company's present production facility is able to handle supplying the current demand, the same cannot handle expansion in the same building. The owner is facing the question of whether it is time to buy another production facility. To help him in coming up with the right decision, he plans on preparing projected financial statements and conduct internal and external analyses.

Elizabeth M.A. Grasby; Richie Bloomfield

Harvard Business Review (W16729-PDF-ENG)

November 10, 2016

Case questions answered:

- Identify trends in the chocolate manufacturing industry. How do these trends affect Habitual and its future decisions?

- Who are Habitual’s customers? What do they want? Which customer base should Habitual target?

- Who are Habitual’s most important competitors? What is Habitual’s competitive advantage? Is it a sustainable advantage?

- Assess Habitual’s qualitative corporate capabilities.

- Create a statement of cash flow for fiscal 2014. Was a positive cash flow generated from operations? What are the largest sources and uses of cash? Is Habitual doing a good job of matching its sources and uses of cash?

- Calculate the most important ratios for Habitual. How do these ratios compare, year over year? How do they compare to the industry?

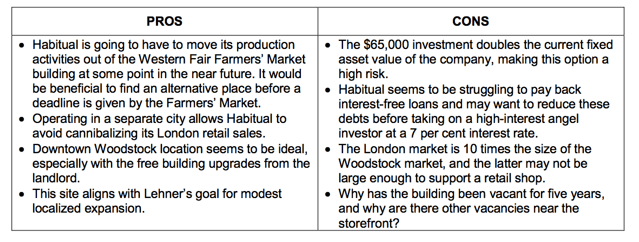

- Identify qualitative pros and cons of the expansion into Woodstock. Is this a good opportunity for Habitual, given its current position?

- Prepare a differential analysis. Calculate the return on investment (ROI) and payback for the Woodstock store launch (as compared to the status quo) using the high and low estimates given in the case. What conclusions can be drawn from this analysis?

- Based on your decision(s), prepare a projected statement of earnings for Habitual.

- Prepare a three-month cash budget.

- Prepare a projected statement of financial position.

- As Philippe Lehner, create an action plan based on your decision(s). Focus on the most important risks that Lehner will face if he proceeds with your decision and on how he could best mitigate those risks.

Not the questions you were looking for? Submit your own questions & get answers.

Habitual Chocolate: Expansion Opportunities Case Answers

1. Identify trends in the chocolate manufacturing industry. How do these trends affect Habitual Chocolate and its future decisions?

External Analysis

Habitual Chocolate competes in the chocolate manufacturing and retailing industries, and smaller companies, profitability can be hard to achieve.

This aspect of the industry is supported by the rapid push towards mechanized efficiency in large-scale production, which has led to consolidation in the industry and greater disparity in volume and, therefore, economies of scale between the large and small industry players.

Furthermore, commodity price and exchange rate fluctuations heavily influence producers’ cost of inputs but are largely unpredictable and entirely external.

Smaller companies must find a way to either diversify their product offerings or find a niche market to charge a higher price to increase their margins.

The industry had seen much stronger growth than the manufacturing industry in general, but this growth was expected to stagnate with the macroeconomy.

Given this slow growth and the aforementioned high-risk variables, the timing is poor for a company to expand within the chocolate manufacturing industry.

Finally, current health trends do not favor an industry whose products are mostly labeled as “a treat;” however, dark chocolate products seem to be the exception to this trend.

The push for efficiency will be challenging for an authentic artisan producer due to the extremely lengthy natural production process, which can be almost 20 times as long as large competitors’ mass production processes.

This aspect will also strain cash flow and the ability to meet peak demand on short notice.

2. Who are Habitual’s customers? What do they want? Which customer base should Habitual Chocolate target?

The case provides information about two demographic groups: young professionals and retirees. The two consumer groups are attracted to Habitual for fundamentally different reasons.

The young professionals are drawn to ethical purchases at a higher price point. At the same time, retirees are willing to pay a premium price for nostalgia (i.e., the “good old days” of hand-crafted chocolate.

Currently, compared to retirees, young professionals make up a much more significant portion of Habitual’s sales figures, so Lehner should focus on the younger group.

Also, young professionals often have higher incomes than retirees. They often spearhead community initiatives (downtown revitalization and Emerging Leaders London) that align with Habitual’s business model.

It is important to note that Woodstock appears to contain a larger percentage of retirees than young professionals. This is concerning, and Lehner should stay in London or perhaps consider a different, larger city center.

If staying in London is suggested as an option, Habitual runs the risk of cannibalizing other London retailers who are its current wholesale customers, and this issue must be addressed.

Remark and Farm Boy could drop their Habitual orders if they notice that demand is dropping due to opening a new Habitual retail shop in London.

Others may argue that a storefront that is open during the daytime in Woodstock would be better suited for the retiree demographic. Even though Woodstock’s population is only a tenth of London’s population, it is far enough away from London to be considered a separate competitive landscape.

3. Who are Habitual’s most important competitors? What is Habitual’s competitive advantage? Is it a sustainable advantage?

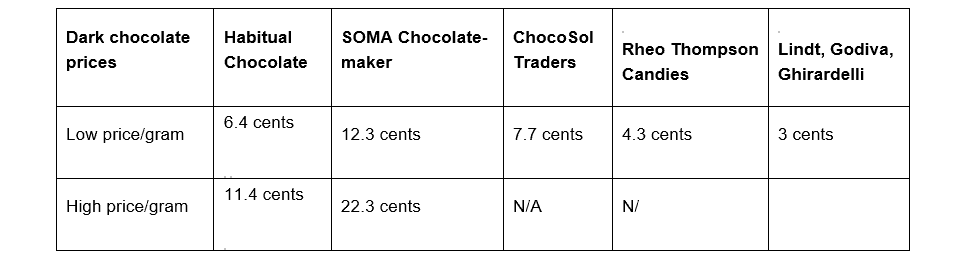

The case provides information on three important local competitors to Habitual: SOMA Chocolatemaker (SOMA), ChocoSol Traders (ChocoSol), and Rheo Thompson Candies (RTC), as well as a summary of major indirect competitors.

Although extensive details have not been provided, some important conclusions can be drawn from the analysis.

Based on its successful expansion across North America and its diverse product offerings, SOMA should be a formidable competitor. Since SOMA is based in Toronto, consumers in the London region may not be as loyal to it as they would be to a London-based company.

It should also be noted that SOMA does not have Fairtrade certification for its products, representing a competitive advantage for Habitual.

Alternatively, the transparency that SOMA provides to its customers may nullify the need for any form of external certification. At the time of the case, SOMA was building an online store, which could provide a further advantage over Habitual.

ChocoSol presents a different competitive threat as a chocolate producer that would be classified as a more socially and ethically conscious industry player compared to SOMA or Habitual Chocolate.

ChocoSol’s business model is centered on long-term, direct relationships with small-scale farmers in Mexico and on rigid, environmentally friendly production processes.

The company’s emphasis on corporate social responsibility may attract more socially conscious consumers; however, it likely prevents ChocoSol from achieving many forms of cost-saving efficiencies that could be reached by producers like SOMA and Habitual Chocolate.

For example, automated production machinery is far less labor-intensive than a pedal-powered machine. Since all of its cacao beans are sourced from one area in Mexico, ChocoSol is at a greater risk of supply shortages due to unpredictable seasonal climates.

Compared to its competitors, RTC is a better-established and much larger company in terms of sales volume, but it has still managed to keep its branding tied to a local artisanal message.

RTC is not as much of a direct competitive threat as ChocoSol and SOMA because RTC does not offer Certified Organic or Fairtrade-certified products.

Many of the consumers who choose these types of products would be likely to bypass any non-certified product. RTC has a less trendy target message and would be more likely to appeal to an older demographic.

Other large chocolate companies that dominate a significant portion of the Canadian market share sell their products targeted to a broad mass market of consumers who want affordable, tasty chocolate.

This factor does not represent a large concern for Habitual since the company is not attempting to attract this group of consumers or meet this scale of the chocolate market.

Overall, aggressive growth is not the primary objective. Habitual should not be overly concerned about the size advantages of some of its competitors.

Rather, it should focus on Greater London, Ontario, market and improve on its niche strengths. The table below provides a comparison of the unit retail prices for dark chocolate across all competitors mentioned in the case.

4. Assess Habitual’s qualitative corporate capabilities.

Internal Analysis

Although Habitual is a relatively new company in only its sixth year of operations, the recent buyout by Lehner provides Habitual with potential growth options that were not previously possible as a subsidiary of Fire Roasted.

The benefits that Habitual gained from its beginnings as part of Fire Roasted, namely, instant access to the retail market that other startup chocolate producers would not have, as well as significant capital support for purchasing expensive machinery.

The loans from Fire Roasted remain interest-free, which significantly benefits the solvency of the young company.

Habitual offers a healthy product when compared to other candy or chocolate on the market. This trait should allow Habitual to associate its products with positive health benefits, such as antioxidant cleansing and improved memory.

Lehner has over 15 years of industry experience, and seven of those years have been spent in Ontario. Lehner’s passion for chocolate “made from scratch” is a perfect match with Habitual, but some may be concerned with Lehner’s lack of business education and experience.

Lehner has no educational business background. It’s a concern if he will be able to cope with the dual role of being a full-time chocolatier and a full-time business manager if Habitual moves forward and expands its operations.

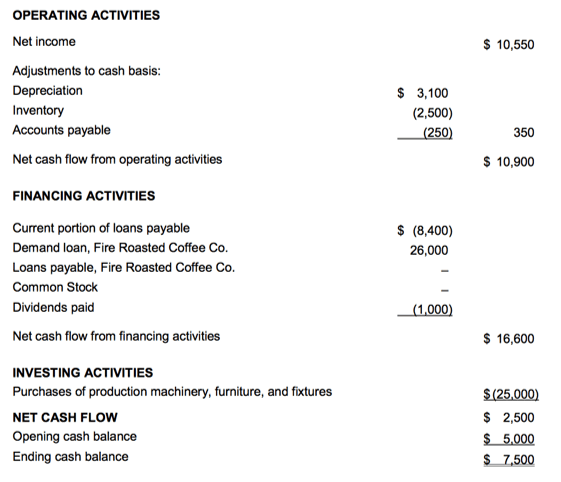

5. Create a statement of cash flow for fiscal 2014. Was a positive cash flow generated from operations? What are the largest sources and uses of cash? Is Habitual doing a good job of matching its sources and uses of cash?

The completed statement of cash flows for fiscal 2014 can be found in Exhibits TN-1 and TN-2.

Most of the analysis of this statement can be broken into three categories: operating activities, largest sources and uses, and the company’s ability to match its long-term sources with long-term uses.

Habitual Chocolate generated positive cash flow from operating activities, and most of this cash flow came from net income, proving that the business model is sustainably creating cash.

The remaining sources and uses in the operating activities section should be expected for a young, growing company. The largest sources of cash were net income and a short-term loan from Fire Roasted.

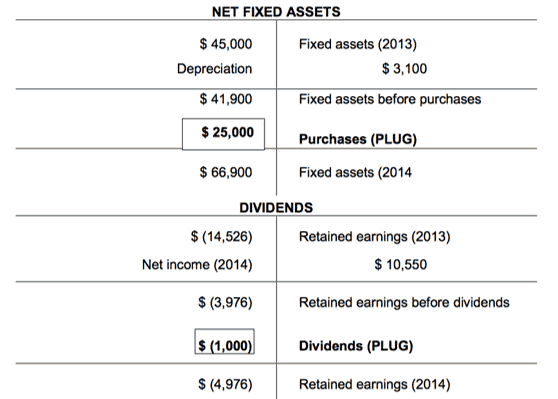

The largest uses of cash are machinery purchases and the payment of long-term loans. It is a positive sign that Habitual can pay back debt while remaining cash-flow positive, but they may question why such a significant amount was paid at the same time as a $26,000 short-term loan was accumulated.

Also, it should be expected that a company with as high a growth as Habitual would invest in new assets at a much faster rate than the value depreciated annually.

Habitual is not doing a good job of matching its sources and uses of cash since it appears that most of the long-term investments were purchased with cash from a short-term loan.

$1,000 worth of dividends were paid out in fiscal 2014 despite a negative retained earnings figure. Habitual Chocolate does have positive shareholders’ equity and can, therefore, issue these dividends; however, the money could have been reinvested in the company at this stage of high growth.

6. Calculate the most important ratios for Habitual. How do these ratios compare, year over year? How do they compare to the industry?

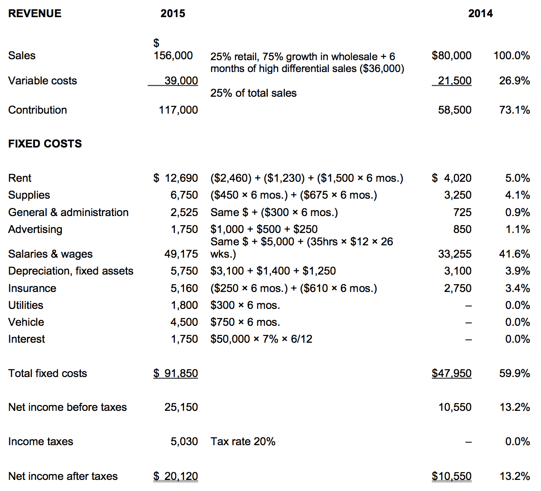

Habitual’s return on assets has improved considerably from −1.8 percent in fiscal 2013 to 12.9 percent in fiscal 2014. This number is now comparable with competitors in the chocolate manufacturing industry and should be a good sign for future long-term asset investments.

The company’s vertical analysis reveals that Habitual is again performing well. Net income to sales in 2014 was above industry numbers, and the trend was positive compared to 2013.

Besides, Habitual’s gross margin is substantially outperforming industry numbers, and this result was likely related to a premium price rather than to cost controls.

The company’s current ratio was cut nearly in half despite a higher cash balance at the end of fiscal 2014. The ratio has fallen significantly below the benchmark of 1:1.

In other words, Habitual would not be able to pay off all short-term liabilities if these loans were called in immediately. This drop in liquidity is mostly due to the $26,000 short-term loan Habitual took from Fire Roasted in 2014, which funded long-term assets. This management decision is a questionable one.

Days of accounts payable were abnormally short in 2014. Therefore, Habitual should take more time to pay back suppliers to free up more cash flow.

The company’s inventory is high when compared to the industry. Still, this issue is unlikely to be significant for Habitual since the inventory (raw cacao beans and organic sugar cane) has a reasonably long shelf life.

As a small artisanal producer, Habitual is also unable to react to seasonality increases or unexpected demand spikes due to limited production capacity and a lengthy production process, which can take up to 76 hours to complete quickly.

Therefore, Habitual must anticipate these events by overproducing during slower periods of sales.

Finally, sales growth is rapid at Habitual since it is a company in its early development stages. This rapid growth rate is a good sign for future profitability if sales can grow at a rate well above the industry average until a more stable brand can be established.

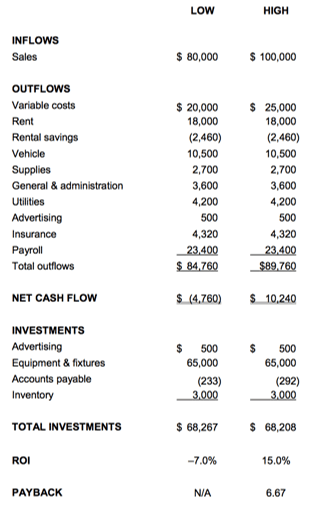

8. Prepare a differential analysis. Calculate the return on investment (ROI) and payback for the Woodstock store launch (compared to the status quo) using the high and low estimates given in the case. What conclusions can be drawn from this analysis?

Exhibit 4 provides a completed differential analysis. Lehner provided both low and high sales scenarios in the case, and both should be projected.

The low sales scenario results in a -7.0 percent return on investment and, therefore, no payback; the high sales scenario provides a 15 percent return on investment and a 6.67-year payback.

Since the equipment and fixtures have a useful life of 15 years, the less-than-five-year payback in the high-sales scenario is reasonable. Overall, the returns are fairly low and will likely be seen as high risk.

9. Based on your decision(s), prepare a projected statement of earnings for Habitual.

See Exhibits 5 to 8.

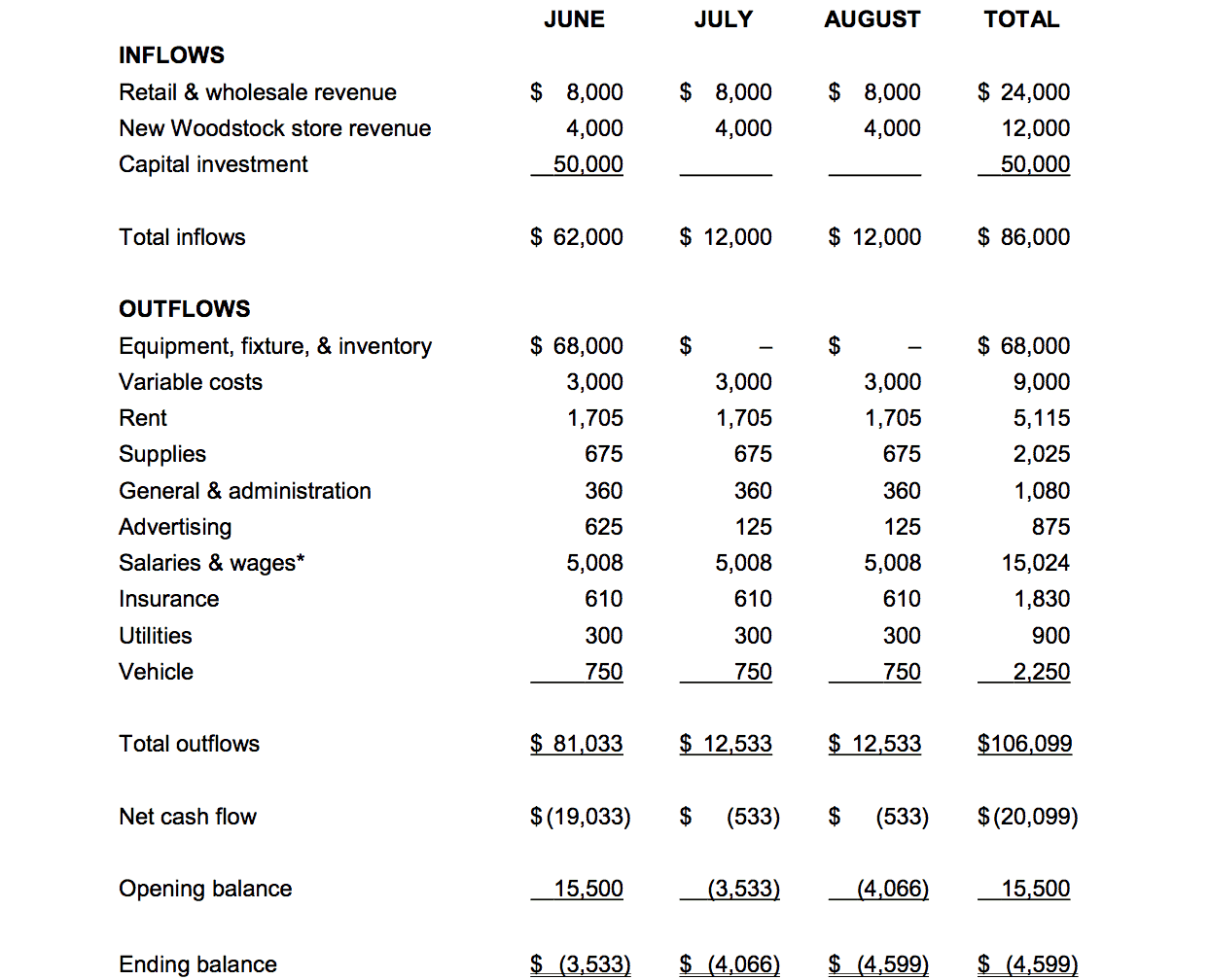

10. Prepare a three-month cash budget.

Depending on the decision they make, HC must assess (1) whether Lehner can pay $2,500 monthly to Fire Roasted starting July 2015 or (2) whether the $2,500 overdraft limit is sufficient to cover the cash shortages during the summer.

Habitual Chocolate should be able to make the payments to Fire Roasted without much difficulty. In both the low and high expansion sales scenarios, Habitual’s overdraft limit will be exceeded, and Habitual should talk to the bank about a higher limit (see Exhibit 10).

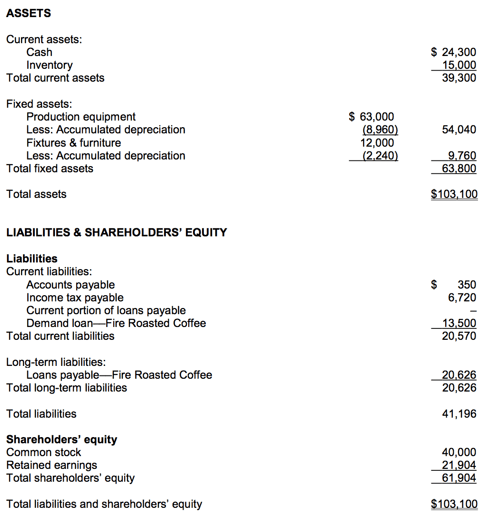

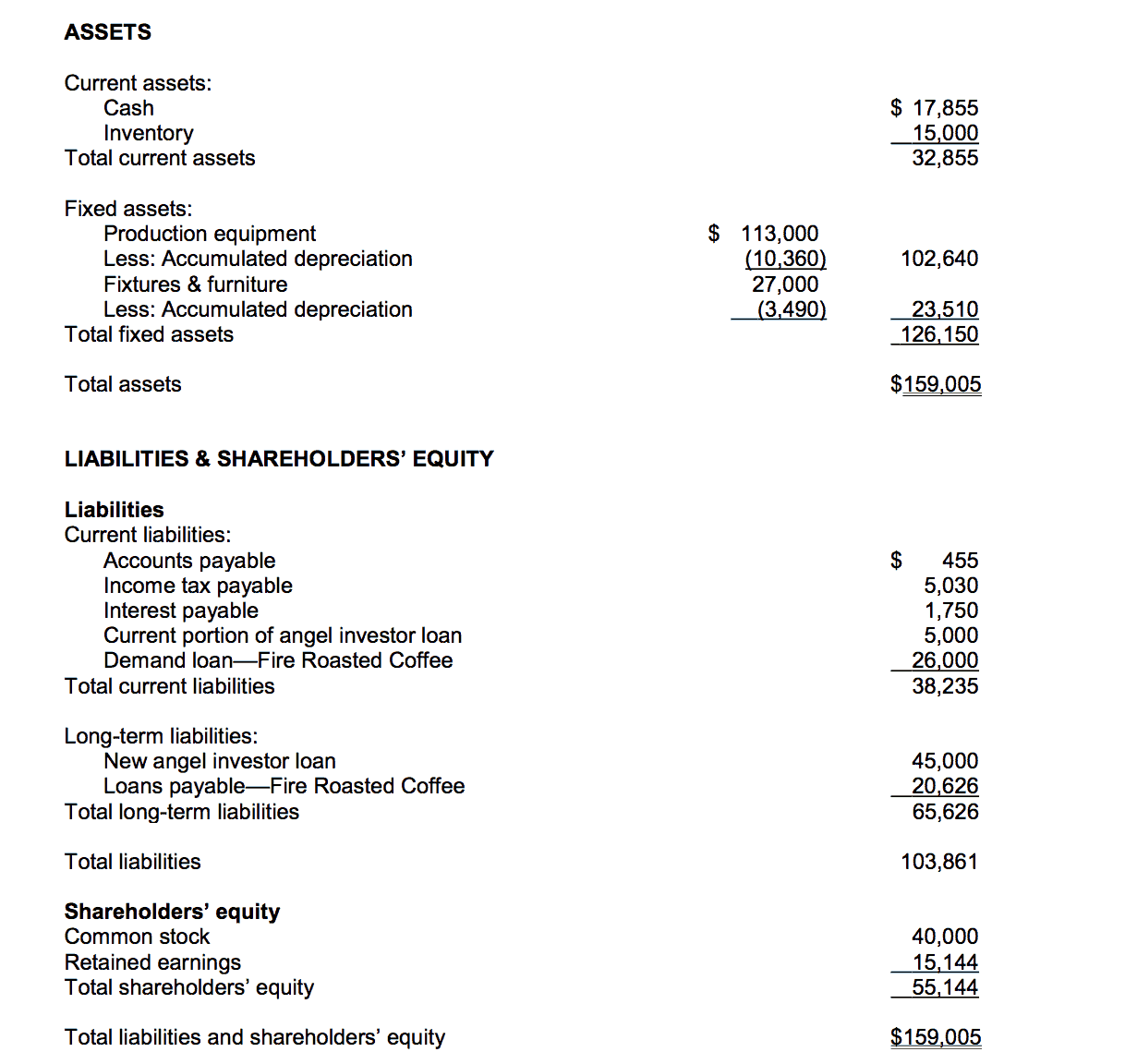

11. Prepare a projected statement of financial position.

Exhibit 11 shows a projected statement of the financial position of Habitual.

12. As Philippe Lehner, create an action plan based on your decision(s). Focus on the most important risks that Lehner will face if he proceeds with your decision and how he could best mitigate those risks.

If Habitual Chocolate decides to open the Woodstock store, Lehner will need to perform the following tasks to complete this expansion:

- Sign the lease and ensure that construction can be completed in time for a grand opening in June 2015.

- Obtain the $50,000 in cash from the angel investor and immediately purchase the new equipment and fixtures for the new store.

- Prepare for the transition of production from London to Woodstock, which likely requires a buildup of finished goods inventory to buffer shut-down production time.

- Create a promotional plan for launching in a new city.

- Hire a new staff member to run the retail store.

If habitual moves, the following issues could arise:

- Lehner cannot purchase new equipment in time for the opening of the new store, resulting in delayed revenue and unavoidable fixed costs.

- Expansion ends up creating too much of a burden for Lehner to manage the business side of things and chocolate production.

- Woodstock’s population ends up being too small to create the estimated sales figures, making the new venture unsustainable.

- The angel investor decides that interest payments should be made right away, putting further strain on cash.

Exhibit 1:

Exhibit 2:

Exhibit 3:

Exhibit 4:

Exhibit 5:

Exhibit 6:

Exhibit 7:

Exhibit 8:

Did this solution help you?

(3 votes, average: 4.33 out of 5)

(3 votes, average: 4.33 out of 5)