Founder and CEO of Medfield Pharmaceuticals Susan Johnson is challenged with the conflicting recommendations on whether to extend the patent life of Fleximat, the key product of the company. The decision is important since it is part of the strategic management of the company's product pipeline. However, this was made more challenging by a $750 million offer for the purchase of the company. Johnson had to make her decision but not before checking the value of Medfield Pharmaceuticals and its existing and potential future products.

Marc Lipson; Jenny Mead; Jared Harris

Harvard Business Review (UV5632-PDF-ENG)

November 14, 2011

Case questions answered:

Evaluate how Medfield Pharmaceuticals should best extend its key drug’s patent life and how to respond to the takeover offer.

Not the questions you were looking for? Submit your own questions & get answers.

Medfield Pharmaceuticals Case Answers

This case solution includes an Excel file with calculations.

Executive Summary – Medfield Pharmaceuticals

The CEO of Medfield Pharmaceuticals, Susan Johnson, is considering whether the firm should extend the patent life of Fleximat, the firm’s key drug, and how the firm should respond to a $750M takeover offer.

These decisions are not only a matter of financial value but also a matter of ethical issues and the firm’s core mission.

After conducting both qualitative and quantitative analysis, I recommend that Medfield Pharmaceuticals drop the offer and reformulate its key drug with substantial changes that benefit patients.

Forecasting risk – Cash flow key drivers: Sensitivity analysis (Exhibit 1) reveals that the estimated sales of Reximet, Cost of sales, Direct Marketing, and WACC have the most impact on Medfield Pharmaceuticals’ cash flow.

While historical financial statements and case information can justify the inputs of the Cost of sales, Direct Marketing, and WACC, there is no solid evidence to justify the sales of Reximet at $80M in the first year. Therefore, the estimated sales of Reximet can pose a forecasting risk to Medfield’s cash flow.

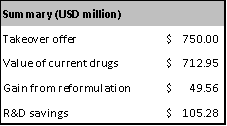

Takeover offer evaluation – To sell or not to sell

1. Value of current drugs: The NPV of current drugs of Medfield Pharmaceuticals is $713M (Exhibit 2). R&D cost is excluded from the calculation since this is a future investment (without cash inflow from new drugs) and not associated with current drugs.

Terminal value is not included as well since there is no evidence for steady growth after the year 2034 or in the long term.

2. Gain from re…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!