This case study discusses the event where Merck & Co. was approached by LAB Pharmaceuticals for a prospective licensing deal for a newly developed drug compound called Davanrik. It looks into the value of the proposed deal.

Richard S. Ruback and David Krieger

Harvard Business Review (201023-PDF-ENG)

October 30, 2000

Case questions answered:

- How has Merck & Co. been able to achieve substantial returns to capital given the high costs and lengthy time to develop a drug?

- Build a decision tree that shows the cash flows and probabilities at all stages of the FDA approval process.

- Should Merck bid to license Davanrik? How much should they pay?

- What is the expected value of the licensing arrangement to LAB? Assume a 5% royalty fee on any cash flows that Merck receives from Davanrik after a successful launch.

Not the questions you were looking for? Submit your own questions & get answers.

Merck & Co.: Evaluating a Drug Licensing Opportunity Case Answers

This case solution includes an Excel file with calculations.

Introduction – Merck & Co.

Merck & Co. Inc. (Merck) is an international, researched-based pharmaceutical company that has been in the business for a while and has been running successfully. At the time, patents for the company’s most popular drugs, such as Pepcid, Prinivil, Vasotec, and Mevacor, were due to expire in 2002.

Since generic substitutions would essentially replace these compounds, Merck could stand to lose almost 50% of its sales revenue, equating to a $5.7 billion loss, if it did not come up with a new drug to bring to the market.

The company refreshes its product portfolio periodically to have stable cash flows through its internal research as well as through joint ventures with other biotechnology companies.

In 2000, Merck & Co. was approached by LAB Pharmaceuticals for a prospective licensing deal for a newly developed drug compound called Davanrik.

It was initially developed to treat depression, but the preclinical development research revealed that the drug has influential effects on blocking antidepressant receptors as well as blocking the receptor that causes hunger, allowing the compound to be used in depression and obesity treatment.

The company lacked commercialization and marketing experience since none of its drugs had passed the FDA approval process.

With a recent denial from the FDA for another compound, the company was hesitant to issue underpriced equity to finance the three-stage clinical trial process since the stock price dropped by over 30%. In these pharmaceutical licensing deals, the various tasks are divided between the licensor and the licensee.

Merck (the licensor) would be responsible for the approval of Davanrik, its manufacture, and its marketing. They would pay LAB (the licensee) an initial licensing fee, a royalty on all sales, and make additional payments as Davanrik completed each stage of the approval process.

Rich Kender, the Vice President of Financial Evaluation and Analysis at Merck, was working with a team to decide whether the company should license Davanrik.

Merck must also decide and conduct an analysis of how much to bid for the license and the potential of failure/success of the drug through the seven-year FDA approval process. The drug would have ten years of commercial life, after which the drug would have little to no value.

The paper is prepared to explain the business model of Merck and the reasons for its success in the pharmaceutical industry. Moreover, it also evaluates the financial potential of Davanrik using decision trees for both Merck and LAB Pharmaceuticals with recommendations on whether to pursue the licensing deal or not.

Merck & Co.’s Business Model

Merck & Co. is in the business of developing compounds for pharmaceutical drugs. The required research and development efforts preceding the launch of a successful blockbuster drug is an extensive and lengthy process and is, therefore, a very expensive one. Nevertheless, Merck & Co. has proven perfectly capable of achieving high returns on capital. The return on assets (ROA) has averaged about 16.5% over the last two years. This is a result of numerous factors.

First of all, Merck has been able to generate tremendous amounts of sales. Since 1995, Merck has launched 15 new products, resulting in sales of $32.7 billion in 1999, which includes $15.2 billion in pharmaceutical benefit management services (PBM) sales.

Since Merck has a well-diversified portfolio of drugs, its four most popular drugs only account for 17% of sales. Some of these products were developed through joint ventures, allowing for a division of costs but also future revenues. This is evident through the moderate share of costs of goods sold in the sales structure (around 50%).

Furthermore, these new products are protected by law under patents, which gives Merck exclusive rights to production and sales. The company utilizes this opportunity to maximize the revenues, after which other companies can produce substitutes that push the profit margins down.

The company, therefore, is always on the lookout for additions to its product portfolio. Merck is also diversified in terms of business lines since it discovers, develops, licenses, and manufactures drugs for commercial use for humans and pets.

The valuation of a pharmaceutical licensing deal varies from that of a generic valuation technique. The differences are due to the fact that the drugs that are in the initial stages of clinical trials would have significantly negative cash flows prior to the approval of a drug.

In other cases, there is historical information about revenues that can then be used to forecast future cash flows. Since pharmaceutical cash flows are risky, the risk can be characterized based on the stage of development.

Risk-Adjusted NPV (rNPV) is a risk-weighted NPV that is widely used in assessing risky projects. It involves forecasting the revenues, costs, and their respective timing but additionally requires the relevant success rate for each stage of development. To account for risk, the expected net cash flow for a given time period is multiplied by the probability of it occurring.

The appropriate probability of success depends on the drug’s therapeutic area and stage of development. Once the net cash flow of each time period has been correctly risk-adjusted, these cash flows are then discounted using an appropriate discount rate. As most of the pharmaceutical revenue forecasts are real, the appropriate discount rate is the real discount rate.

In order to visualize the different stages of the FDA approval process with its likelihood and expected cash flows for Merck, a decision tree has been constructed. It is a decision support tool mostly used in decision analysis.

Merck’s Decision Tree

The decision tree for Merck & Co. can be found in Appendix I. As can be seen, the tree starts with the decision to license and begin Phase I with an initial cost of $30 million (including a $5 million licensing fee) with a 60% probability of success.

The alternative decision is to not license the drug. If Phase I is successful, Phase II trials start. This phase has a cost of $40 million with different probabilities of success. The probability of success as a depression medication is 10%.

For the drug to have a positive impact as a weight loss medication, the chances are 15%, and the probability of the drug successfully treating both depression and weight loss is 5%. The probability of passing Phase II is significantly low since it is administered to many people as compared to the Phase I trial.

If any of these outcomes are successful, testing begins in Phase III. Depending on the result of Phase II, each of Phase III possible outcomes has its own cost and probability of success. If phase III is successful, Merck will spend more money to commercialize the drug so that it can be marketed. In this case, the total cost of the whole phase will consist not only of the Phase III cost but also of the product launching cost.

All of the cash flows and probabilities have been taken into account in order to estimate the expected value of each possible outcome. For example, in order to calculate the expected value of the first possible outcome where the drug is only found to treat depression and is launched commercially, the cash flow was calculated as a commercialization present value minus total costs incurred.

Also, the total probability was calculated as a multiple of probabilities in each phase. Similar calculations were done for each branch, including those with failure as an outcome.

The decision tree provides a compelling argument for Merck & Co. to act upon it and move forward to acquire the license of Davanrik. With an NPV of $13.98 million, the benefits outweigh the associated risks of licensing the drug. The product portfolio, with the addition of Davanrik, would provide the company with the likelihood of higher future revenues.

Currently, Merck & Co. is considering paying the licensee $5 million to acquire the license since the initial payment upon the initiation of phase I is considered the amount paid out for the acquisition of the license.

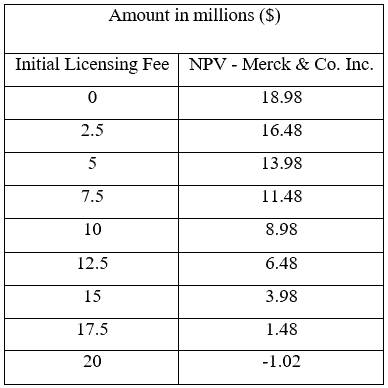

A sensitivity analysis was conducted to look into the different payment amounts and the respective value it would have for Merck & Co. to recommend Kinder and his team about the price they should pay for the license. The sensitivity analysis is provided in Table 1.

Table 1 – Sensitivity analysis

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!