In 2001, Allianz Capital Partners and Goldman Sachs acquired majority stock share in Messer Griesheim (MG), German industrial gas company. The deal characterized the delicate nature of specific governance aspects of a family-operated business. The family wishes to retain company control and the deal makers were aware of this fact. Owing to diversified business operation in multiple geographies, much-needed expertise in the local market, the business controlled by centralized managing committees, MG was facing principal-agent and principal-principal relationship issues. Some plants/units of the company were profitable and lucrative to strategic buyers. Partial business operation buy-out was not beneficial to buyers, also any buyout/sell option was complicated by European anti-trust laws.

Josh Lerner; Ann-Kristin Achleitner; Eva Nathusius; Kerry Herman

Harvard Business Review (809056-PDF-ENG)

February 18, 2009

Case questions answered:

The case study explores the steps taken by the private equity investors to restructure the firm and the relationship the partners forged with the family owners to bring about a favorable exit for the private equity partners and ownership for the Messer family.

Not the questions you were looking for? Submit your own questions & get answers.

Messer Griesheim (A) Case Answers

Case Overview – Messer Griesheim (A)

In 2001, private equity players ACP/GS acquired a 66.2% share in Messer Griesheim (MG), a German industrial gas company. The deal characterized the delicate nature of specific governance aspects of private equity-backed family business operations.

Dealmakers were aware of the family’s wish to retain company control. Owing to diversified business operations in multiple geographies, much-needed expertise in the local market, and a business controlled by centralized managing committees, MG was facing principal-agent and principal-principal relationship issues.

Some plants/units of the company were profitable and lucrative to strategic buyers. Partial business operation buy-out was not beneficial to buyers. Also, any buyout/sell option was complicated by European anti-trust laws.

The case evaluates the strategic steps taken by the private equity investors to restructure the firm and to bring about a viable exit for the private equity partners.

As PE players wanted to move out of business (as per the original deal), the following options were available to the family (having Veto rights).

- Family exercising Call option to buy back shares

- Sell PE share of business in the open market via IPO.

- Divest the German operation of the business to a strategic buyer

Business Analysis/Problems Description – Messer Griesheim Business Operation

Expertise needed in Local operation

Messer Griesheim has diversified operations to gas production from equipment manufacturing, which, apart from capital expenses, possesses gas transportation issues.

To create synergy and add value to the system, logistics/transport/local market information is needed; the complete Supply chain needs to work in tandem.

Principal – Agent Issue

Since business management is done from a centralized source (Supervisory/Shareholder committee) and MG has a diversified business portfolio, it is difficult to control complete business centrally. (Fact not directly available in the case, inferred from reading).

Principal – Principal Issue

During the period under which Hoechst held 2/3 of the shares, the family held 1/3 of the shares, the Hoechst exercised unraveled control over the business. Dorman, CEO of Hoechst, made an over-optimistic investment on several occasions without taking cognizance of the views of the family.

There was growing discontent in the family because of Hoechst’s haphazard expansion based on false investment analysis and planning.

Also, there was a mismatch between Aventis and the objective of Messer Griesheim regarding the divestment of Aventis shares; the family was looking for an ideal partner, while Aventis just wanted to get the highest price.

Spin-Off Effect with Carlyle Group

MEC Holding was created by divesting MG electric welding, filler material, and cutting business in Europe (in collaboration with Carlyle Group). It served as a dry run with family experience with private equity partners.

MG desires to control the operational part.

While being a partner with Hoechst, the family exercised less control over the operation of the company. Hoechst, a pharmaceutical company, did not have expertise in the gas business.

The collaboration did not work in favor of the family. With PE as a partner, the company exercised better control over operational/managerial decisions.

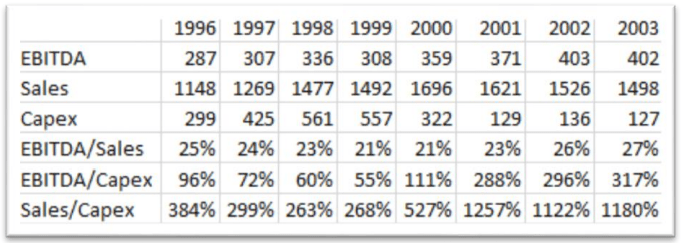

Effect of Consolidation from 2000-2003

EBITDA/CAPEX, Company Debt, and employee productivity have improved compared to the diversification phase (1995-1999).

Clearly, with the consolidation of business, Financial ratios such as EBITDA/Sales, EBITDA/ Capex, and Sales/ Capex are improving from 2001-2003. So, PE collaboration has been beneficial for the company.

Option1 Analysis – Family exercising Call option to buy back shares

The call option puts Messer Griesheim perfectly in a safe spot, considering that ACP and Goldman Sachs offer a steady IRR. This would include the chance that the company is saved and the chance that the Messer family could take over the shares of a company at a better stage.

Advantages:

The company seems to be in a better position from 2000 to 2003, as indicated by the following parameters:

- Infusion of capital worth 392m from 2001 to 2003

- Decrease in debt from 1627m Euros in 2000 to 1117m Euros in 2003.

- Long-term employees are content with the return of old management

Challenges:

- The company cannot exercise the call option in its entirety without debt.

- The company has no particular strategy in place to work with after exercising the call option.

Option 2 Analysis- Sell PE share of business in the Open Market via IPO.

Business is fragmented, with some operations/plant locations profitable while other locations are not lucrative to buyers. Messer Griesheim still has highly leveraged operations. So, in an open market, GS/ACP is not getting a good price value (66% of business is going for IPO).

Since the family wants to retain control of the German operation, it is difficult to divest the company in parts. The company is also looking for a credible buyer, has firm European roots, and has resistance to selling its business operation to any other buyer from the market. So, this option is not feasible both from a family and PE perspective.

Option 3 Analysis – Sell the company to a strategic buyer.

Buyers were willing to pay a premium, which IPO was unlikely to offer. Possible reasons could be:

- Strategic buyers pay for the readily available synergies that can be used for vertical or horizontal expansion since certain areas of the Messer Griesheim business were profitable. The company’s German business was lucrative.

- At that time, there were no substitutes for the Industrial gases market. Hence, premium pricing could be charged.

- The CAGR of Net Debt from 2000 to 2003 was 11.8%. Strategic buyers are probably large companies with access to capital and would find it easy to service and repay the company’s debt easily. A huge debt would not go down well with a financial buyer, who would be more interested in returns.

A strategic buyer pays a premium price because of the far-sighted opportunities in expanding a business. However, sellers need to make concessions for the high price.

Did this solution help you?

(6 votes, average: 2.83 out of 5)

(6 votes, average: 2.83 out of 5)