John Hansen is the CEO of Metapath Software, a provider of software and services to wireless carriers. In September 1997, Hansen held a board meeting to decide on two offers. One was a proposal by CellTech Communications, a wireless products company with a market capitalization of approximately $260 million, for acquisition. Under this offer, Metapath's shareholders would get a common stock in CellTech worth $115 million, at closing. The other proposal was for an investor consortium led by Robertson & Stephens Omega Fund and Technology Crossover Ventures. Its intention was to buy $11.75 million of stock at a $76 million pre-money valuation - something much stricter than the terms of the stock owned by existing shareholders.

G. Felda Hardymon; Bill Wasik

Harvard Business Review (899160-PDF-ENG)

January 06, 1999

Case questions answered:

- Analyze Metapath Software’s capital structure, in particular, the various forms and prices of preferred stock from the multiple previous rounds.

Case study questions answered in the second solution:

- Analyze the RSC offer. How much is the participating feature of the Series E Preferred worth? To do so, answer the following questions:

a.) Derive a “Capitalization table” that shows how many shares are owned by the various parties if the RSC offer is accepted.

• Assume that Metapath would raise $10.75M as specified in the term sheet, not the $11.75M as specified in the case.

• Also assume that the terminal payoffs occur in 3 years -before any dividends are actually paid or accumulated.

b.) Describe the payoffs of the proposed Series E Preferred in Exhibit 12.1. Describe the payoffs for both types of possible exit scenarios (Sale or IPO) separately.

c.) What is RSC’s stake worth under each scenario? (Hint: Look at Metrick Chapters 15.2 and 15.3). Consider carefully when each shareholder is going to convert.

d.) Provide a break-even analysis under each scenario. Comment.

e.) How can you get an overall value for the value of RSC’s offer? In particular, what assumption do you need to make in order to get a numerical valuation of the offer? Provide a sensitivity analysis for your results.

f.) Comment on the type of security that RSC is getting. - How do you analyze the CellTech offer? (CellTech=Alpha, Metapath=Zenith) What are the risks for the Metapath shareholders if the board accepts the CellTech offer?

- Compare the two offers. Which one would you recommend to Metapath’s shareholders?

Not the questions you were looking for? Submit your own questions & get answers.

Metapath Software: September 1997 Case Answers

This case solution includes an Excel file with calculations.

You will receive access to two case study solutions! The second is not yet visible in the preview.

Executive Summary

Metapath Software, a wireless carrier networks software firm, was formed in 1995 with a joint venture between Networks Northwest and Securicor Telesciences. The firm had, prior to 1997, raised $9 million from four rounds of financing. The company would be looking to go public in a couple of years’ time after sorting out cyclical revenues and dependence on four major customers.

Metapath currently has an acquisition offer from CellTech and an equity financing offer from a venture syndicate led by Robertson and Stephens Omega Fund (RSC). CellTech is a wireless technology hardware vendor that provides value-added services to wireless providers.

CellTech recently went public and has a market cap of $260 million with a positive forecast from financial analysts. The offer laid down by CellTech has an attractive price proposal ($115 million), which is around 45% of CellTech’s market capitalization as of now. High operating and talent synergies are expected for Metapath.

The equity offer from RSC proposes terms to purchase stocks at a $75m pre-money valuation. The proposal includes participating convertible preferred stock like the choice of security, the holder of which gets preference both in liquidation and equity participation at the same time.

The offer yields different payoffs for RSC, given the capitalization structure depending on the exit, IPO, or sale. The RSC’s value of the offer is estimated to be $20.59 million, with break-even values at $27.08 million for sale and $46.16 million for IPO scenario.

The acquisition offer gives Metapath an opportunity to go public one year earlier than expected, yet management believes that they could do well independently and go public on their own in a few years’ time. Moreover, they were unsure about the future performance of CellTech in the stock market. The second offer of equity financing had quite stringent terms when compared to the previous financing rounds.

We believe that RSC was asking for much more than they were willing to give Metapath, compelling management to go public without additional payoff. We recommend John Hansen look out for better financing options with less strict terms that make Metapath’s position attractive enough to go for an IPO in one year’s time.

Case – Metapath Software

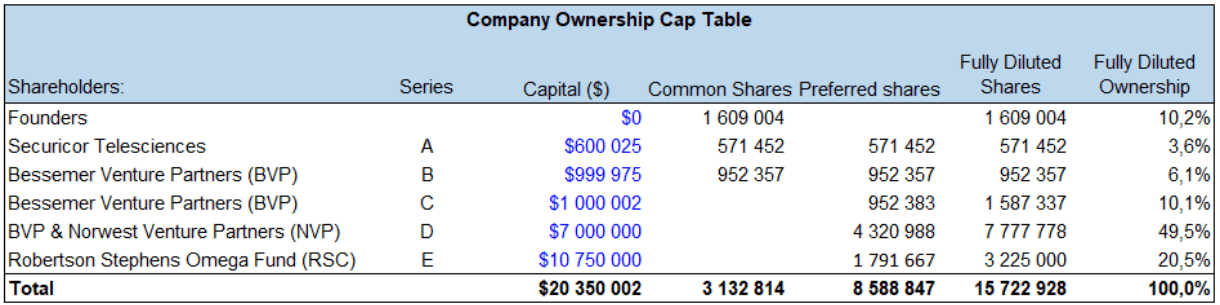

Series E – The RSC Offer

Robertson Stephens Omega Fund (RSC) and a syndicate of other investors offered $10.75m to Metapath in exchange for participating convertible preferred stocks (PCPT) in the company. Their pre-money equity valuation is equal to $76 million for approximately 12.5 million shares outstanding, with a price per share of $6.

If their offer is accepted, Metapath capitalization table will look like this:

Series A and B have common and Preferred shares as a result of the packaged deal mentioned in footnote 2, Exhibit 1 of the case. The exact number of common shares owned by the founders is unknown.

The number (1 609 004) could include various employee stock options. We assume that Series E preferred stocks have the same conversion rate as Series D of 180% since the redemption rights and other terms are mentioned to be similar.

The RSC will own 20.5% of Metapath if they convert their preferred shares. There is no rationale behind not converting them into common stock at any sale price that is higher than $20.35 million as then they would be 20.5% owners of the company, and all excess sale consideration will be divided on a pro-rata basis.

The PCPT instrument gives RSC two different payoffs depending on the exit scenario. In an IPO event, their preferred shares get automatically converted into common stocks at the conversion rate of 180%, giving them 20.5% ownership of the post-IPO value. Accrued dividends pre-IPO will be paid out or owed to RSC.

If Metapath is sold, the payoff for RSC would depend on the…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!