The case study Mumate is a typical scenario of a young firm seeking external financing. In this case, MuMate is already an operating company that would rely on the venture capitalist DuPage Venture (DPV) to finance its expansion and growth possibilities. It looks into how much capital should be invested by DuPage into the company.

Thomas R. Eisenmann and Alex Godden

Harvard Business Review (813085)

January 18, 2013

Case questions answered:

- How much capital should be invested by DuPage into MuMate?

- What is the post-money valuation of MuMate? (post-money valuation = new investment + pre-money valuation)

- What is the appropriate size (from the perspective of your role) of the option pool? (as % of total shares outstanding after the round, including shares reserved for options; assume that the option pool will be created before DuPage invests)

- What is the appropriate board composition for MuMate? (specifically how many seats are to be filled by the VC, by MuMaté cofounders, and by independent directors)

- Any other terms that might be negotiated?

Not the questions you were looking for? Submit your own questions & get answers.

MuMate Case Answers

This case solution includes an Excel file with calculations.

1. Introduction – Mumate Case Study

The case study Mumate written by Eisenmann & Godden (2013), is a typical scenario of a young firm seeking external financing. In this case, MuMate is already an operating company that would rely on the venture capitalist DuPage Venture (DPV) to finance its expansion and growth possibilities. Our point of view is from the venture capitalist.

First, to determine a proposal to MuMate, DPV must value the firm. We have chosen a combination of a DCF bottom-up approach for revenue estimation and a top-down approach for gross margin and expense estimation.

Second, it is fundamental for DPV to determine how to invest in MuMate and for how much.

Third, besides the actual valuation, there also should be considered other negotiation terms between DPV and MuMate. These include the size of the option pool, the board size, the members of the board representing the stakeholders, the voting rights, skills, and experiences of potential members, and a possible board extension in the future.

The purpose of this report is to determine reasonable negotiation terms that yield the best possible return on investment for DPV while also helping MuMate reach its full potential value.

The report starts with the valuation analysis of MuMate. The fourth section analyses the amount and structure of the funding offer. The fifth section focuses on the option pool. The sixth section establishes the best future board composition, and finally, the last section will analyze further negotiation terms to consider.

2. Pre-money valuation

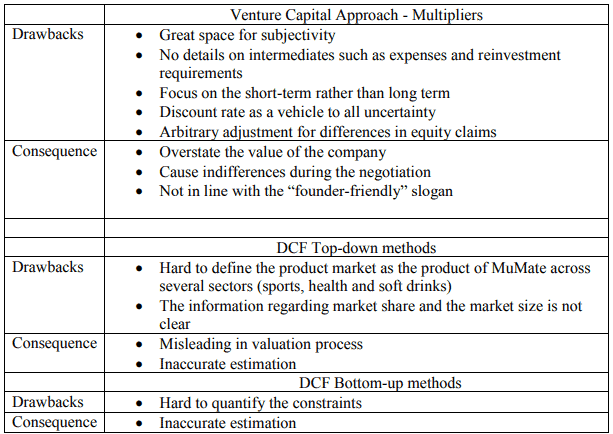

Before DPV makes any investment decisions, we need to accurately value MuMate. Various valuation methods have been used to value start-ups, such as the Venture Capital (VC) Valuation method, the Discounted Cash Flow (DCF) Bottom-up method, and the Top-down method.

After comparing these methods and evaluating MuMate’s situation (see the comparison in Appendix A), we have chosen a combination of the DCF bottom-up approach and Top-down approach for the following reasons (Damodaran, 2009).

Appendix A: Descriptive summary of valuation methods

Firstly, DCF methods contain operating and financing information estimations based on the firm’s condition. It does not allow too much subjectivity.

Secondly, it is more accurate because it does not only consider the revenue and earnings, unlike the VC method, but also takes intermediates such as operating expenses and reinvestment requirements into account.

Thirdly, the DCF method is based on long-term valuation with emphasis on the time value of money. Apart from the discount rate, other vehicles, such as survival rates, are adopted as well to cope with the uncertainties involved in start-ups.

The DCF approach also allows more rigorous adjustments for differences in the equity claims.

Finally, Ms. Maxwell, one of the founders of MuMate, has estimated revenue and sales growth based on weekly volumes, recent sales, and information from distributors about similar firms (Bottom-up).

On the other hand, the operating margin and various costs were estimated with a certain percentage of sales (Top-down). We assume the estimations of operating margin and expenses are valid based on MuMate’s current performance, considering that MuMate reached a turnover of $3 million without external investments and is on track to achieve its projected revenue in 2012.

However, we have decided to adjust the final valuation using an expected survival rate. It is uncertain whether the current popularity of MuMaté will remain in the fast-changing beverage market (Knaup & Piazza, 2005, 2008, as cited in Damodaran, 2009).

2.1. Revenue, gross margin, and expenses

We projected the profit and loss statement (Table 1) for MuMate from 2012 to 2020 and its terminal value afterward. The first step of our valuation is estimating revenues.

Ms. Maxwell estimated that the revenue of MuMate would grow to $50 million in 2015 and grow for an additional five years, with a 10% to 20% growth rate. Assuming that MuMate has a 15% (average of her estimation) growth rate, the company would reach $100 million in 2020. This is not realistic, as only 3-4 out of 2000 beverage brands can reach the expected sales of $100 million.

On the other hand, MuMate did survive the most demanding phase of the “new product winnowing process.” Therefore, we assume the lower limit of Ms. Maxwell’s estimation of 10% would apply.

Also, we estimate the COGS, G&A expenses, S&M expenses, working capital, and tax rate to be 73%, 10%, 11%, and 10% of the revenues, and 34% of the EBIT. The arguments are presented in the notes below in Table 1.

2.2. Discount factor, terminal value, and survival rate

After calculating the free cash flow of MuMate, the next step is to discount the cash flow to its present value. We have adopted a weighted average cost of capital (WACC) in this calculation, as this method is widely used and accepted.

All the formulas to calculate the DCF are presented in Formula Box 1 in the appendix. To conduct this calculation, we have collected relevant figures from various sources, as shown in the notes below, Tables 2, 3, and 4. The cost of capital of MuMate for each year is calculated in Table 4.

In terms of terminal value, we assume MuMate will go public or will be acquired by a publicly traded firm. Thus, we calculate its perpetual growth rate (Damodaran, 2009). The formulas adopted are presented in Formula Box B.

As shown in the overview in Table 5, the terminal growth is calculated to be $35.5 million. The sources of the figures adopted, and details of the calculation are presented in the notes below Table 5.

For the pre-money valuation, we use a general survival rate of 50% to anticipate MuMate’s overall chance to reach its target…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!