MW Petroleum Corp. is a wholly-owned subsidiary of Amoco Corp. which is considering selling the former to Apache Corp. Apache's possible acquisition presents essential monetary and financing considerations. This case analysis deals with looking into the value of MW Petroleum Corporation using the AVP to calculate the value of MW reserves and conduct an analysis of MW as a portfolio of asset-in-place and options.

Timothy A. Luehrman, Peter Tufano, Barbara D. Wall

Harvard Business School (295029-PDF-ENG)

Nov 7, 1994

Case questions answered:

We have uploaded two case solutions, which both answer the following set of questions:

- Is it reasonable to expect that the MW Petroleum Corp. properties are more valuable to Apache than to Amoco?

- What is the most likely source for the value difference?

- How would you conduct an analysis of MW as a portfolio of asset-in-place and options? Specifically, what parts of the business should be regarded as assets-in-place, and which are options? What kind of options are present? Should this approach yield a higher or lower value than the all APV approach in (2)?

- Perform the analysis you proposed in (3).

- What is the value of asset-in-place?

- What is the value of options? Clearly state and justify all the elements that are necessary for the option valuation.

- How much is the whole portfolio worth based on (a) and (b) above?

- How sensitive is your estimate to the assumptions used?

Not the questions you were looking for? Submit your own questions & get answers.

MW Petroleum Corp. (A) Case Answers

This case solution includes an Excel file with calculations.

You will receive access to two case study solutions! The second is not yet visible in the preview.

Summary – MW Petroleum Corp. (A) Case Study

Apache Corporation was an independent oil and gas company based in Denver and engaged in the exploration, development, and production of oil and natural gas. In late 1990, Apache Corporation began to consider the probability of buying MW Petroleum Corp., a wholly-owned subsidiary of Amoco Production Company, which was an integrated petroleum and chemical company based in Chicago, Illinois.

Our group is to help Apache’s chief financial officer, Mr. Wayne Murdy, decide MW Petroleum Corporation’s value. Our group used AVP to calculate the value of MW reserves. Then, we analyzed MW as a portfolio of assets in place and options. We compared the result with the former APV approach.

Overview

Our group aims to help Apache Corporation evaluate the worth of MW Petroleum Corporation, a subsidiary of Amoco Production Company.

MW Petroleum Corporation is not an important part of Amoco Company, and it is in the middle of the margin curve. However, MW Petroleum Corporation could compensate for the disadvantage of Apache Corporation. So, MW is more valuable to Apache Corporation.

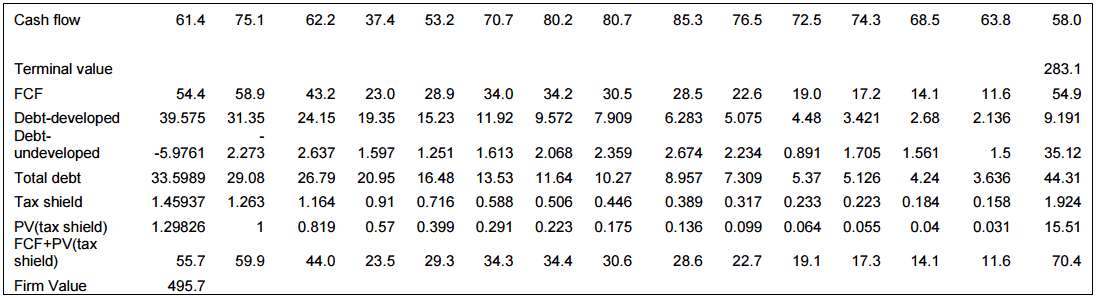

Then, we used the APV approach to calculate the value of MW reserves, which is 495.7, and we analyzed MW as a portfolio of assets in place and options. The whole value of the portfolio is 462.07.

Q1. Is it reasonable to expect that the MW Petroleum Corp. properties are more valuable to Apache than to Amoco?

Yes. We conclude that MW properties are more valuable to Apache.

First, the cost brought by MW to the two firms and size is the first source of the difference. Amoco Corporation, with $28 billion in operating revenues and $1.9 billion in net income, focuses its business on three aspects: oil and gas exploration and production, refining and marketing, and chemical production.

However, MW focuses only on the oil and gas industry, which has a great decade and volatility. The volatile price depressed Amoco, and MW was in the middle section of its margin curve, which is less profitable and more costly for Amoco.

What’s more, the direct operating costs were well-controlled, and it was hard to save in Amoco. Amoco has high overhead expenses, so it’s better for Amoco to divest MW Petroleum Corp. and focus on its attractive properties.

However, Apache is also an independent oil and gas company, and its oil-gas ratio is 20-80, which the gas prices had been extremely volatile, so adding the MW to Apache would shift its ratio to 40- 60, resulting in reducing the great risk of Apache’s revenue stream and promising Apache significant cost-saving opportunities.

Moreover, diversification is the second difference. MW’s holding includes a working interest in the Gulf Coast, Rocky Mountain, and Mid-continent regions and the Permian Basin of Texas and New Mexico; Apache Corporation was based in Denver, Colorado.

So, MW’s properties would further diversify Apache geographically and give the firm future acquisition opportunities. At the same time, Amoco became North America’s largest private holder and producer of natural gas after purchasing Dome Petroleum. As a result, MW is useless for Amoco to great diversification.

Finally, a suitable strategy is another value difference. Apache developed a strategy, “rationalize and reconfigure,” which involved acquiring properties that Apache could control and make more efficient. But MW cannot only double Apache’s reserves but also contain the properties well-suited to Apache’s operating capabilities.

However, as for Amoco, MW is complete with its own reserves and management teams and generates no strategy; thus, MW is not as valuable to Amoco as Apache.

Q2. What is the most likely source for the value difference?

Given that the risk-free rate is 0.0803 and unlevered asset beta is 0.82, and the risk premium is 0.06, we start to find the discount rate Ru = Rf + ß * (R – Rf) = 0.0803 + 0.82 * 0.06 = 12.95%.

Then, we consider Ru as the discount rate to calculate free cash flow. Then, as the maximum loan-to-value ratio is 50% of the value of proved reserves, and based on the assumption that MW Petroleum Corp. has a solid credit rating, we use…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!