Nestlé is composed of 3 businesses in unrelated industries among which no meaningful synergies exist (food & beverages, ophthalmic industry, and cosmetics). The industries adhere to very different dynamics and trends, growth prospects differ and are much higher for Nestlé’s subsidiary Alcon (ophthalmic) than for Nestlé’s core unit, food & beverages. Due to its different units, Nestlé shows conglomerate characteristics and is effectively valued lower than the value of its parts summed up. This is especially problematic, due to the different growth prospects.

Mihir A. Desai; Vincent Dessain; Anders Sjoman

Harvard Business Review (205056-PDF-ENG)

December 08, 2004

Case questions answered:

- Nestlé’s management seems to believe that the stock market is not fully appreciating the company’s intrinsic value. Why are analysts potentially ignoring the full value potential of Alcon? Does the Nestlé group have conglomerate characteristics?

- Is Nestlé effectively trading at a conglomerate discount? Please quantify. Note: assume the $9,1000m valuation for the L’Oreal stake.

- The traditional way of solving a conglomerate discount issue is to sell or spin-off subsidiaries rather than carving them out. From the pure perspective of solving the conglomerate discount issue, compare the pros and cons of the three alternatives.

- What other reasons may Nestlé have to prefer the equity carve-out solution?

- Putting everything together, what are the pros and cons, from the perspective of Nestlé’s shareholders, of going ahead with such a transaction?

- Please compare the four alternatives to list Alcon’s shares. What are the pros and cons of each? Which would you recommend?

- What would be a fair price for Alcon’s shares at the IPO? What should be the minimum IPO price acceptable to Nestlé?

Not the questions you were looking for? Submit your own questions & get answers.

Nestle and Alcon--the Value of a Listing Case Answers

This case solution includes an Excel file with calculations.

Executive summary

Nestle Conglomerate

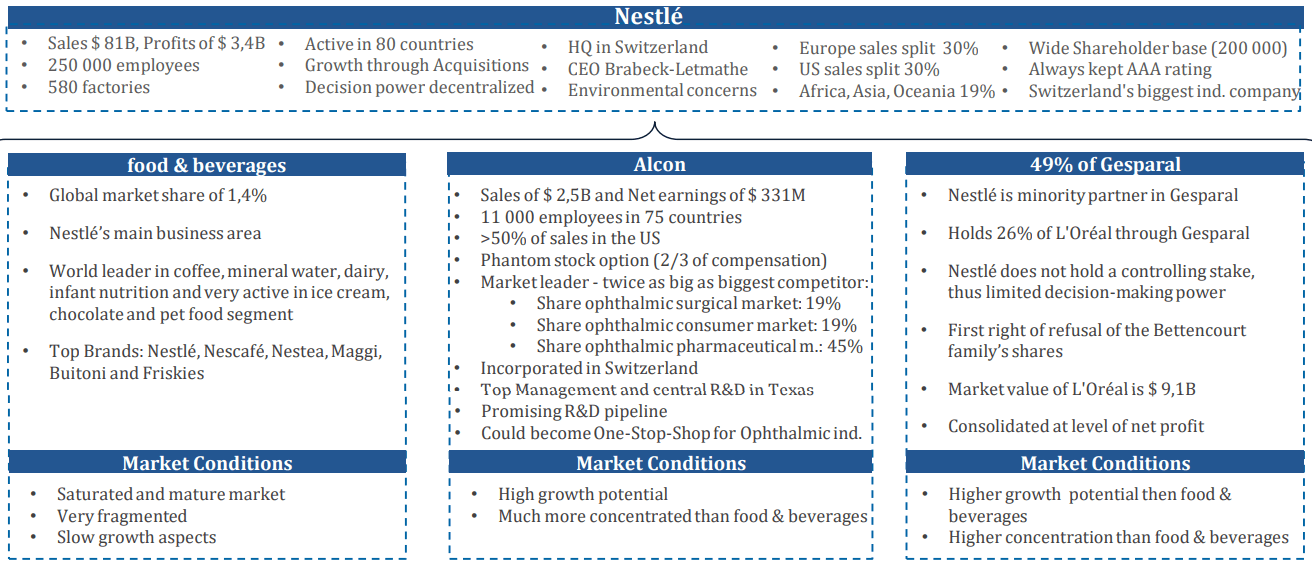

Nestle consists of 3 businesses in unrelated industries, among which no meaningful synergies exist (food & beverages, ophthalmic industry, and cosmetics). The industries adhere to very different dynamics and trends, and growth prospects differ and are much higher for Nestlé’s subsidiary Alcon (ophthalmic) than for Nestlé’s core unit, food & beverages.

Due to its different units, Nestlé shows conglomerate characteristics and is effectively valued lower than the value of its parts summed up, i.e., it is traded at a conglomerate discount of 7%. This is mainly due to analysts covering Nestlé not being able to evaluate these different business units correctly, as they are familiar mainly with Nestlé’s core unit, food & beverages.

Nestlé is evaluated with a blended multiple, which thus mainly represents this core unit and does not appropriately reflect the conglomerate’s other operations. This is especially problematic due to the different growth prospects.

Alcon’s EBITDA multiple derived from comparables is about twice as high as the blended multiple with which it is evaluated (suggesting an undervaluation). The blended multiple is also in line with Nestlé’s food & beverage comparables, even though it should be higher given the multiple-increasing effect of Alcon and Gesparal.

Consequently, the food & beverage unit is trading at a discount. Additionally, the conglomerate structure brings lower transparency, higher complexity, and control costs, which usually have adverse effects on valuations.

Sell / Spin-off / Carve-out

In order to dissolve its conglomerate discount, Nestlé has to separate its business units to make them legally independent entities and enable analysts and investors to assess and invest in them separately. Gesparal is already a separate entity in which Nestle only holds a minority stake, so the main issue is with Alcon.

In order to dissolve the discount, 3 options prevail: selling Alcon, spinning it off, or carving it out. Selling would mean selling the whole subsidiary or its assets, ideally at a fair value. Nestle could choose to distribute the cash to its shareholders or reinvest in its core business unit. Spinning off Alcon would mean that a new legal entity is created, and Nestle’s current shareholders would become shareholders of the new Alcon company.

Since Nestle’s shareholders might not be interested in holding Alcon shares (very different from Nestle’s core activities), a spin-off should be accompanied by providing liquidity to the share, i.e., listing. If many shareholders opt to sell their shares, though, the share price will plunge.

Additionally, there is no price established yet in the market for Alcon, which increases uncertainty. In a carve-out, only a part of the company is sold.

Nestle plans on selling a minority stake by listing Alcon, which would imply a minority discount on the share price. However, a carve-out would allow for reducing the conglomerate discount issues (not completely solve them since Nestle is still invested in the Ophthalmic industry) while keeping control and establishing a price in the market. Often, carve-outs are followed by complete divestitures as a next phase to reduce uncertainty.

Alcon IPO

There are 4 main options on where to list Alcon shares: Swiss listing, US listing, Dual listing, and American Depositary Receipts (ADR).

The main considerations in deciding are how to appeal to the right investors and the costs of each option. Given that Alcon is deriving more than 50% of its sales from the US, where its top management and R&D are based, and the great number of potential investors in its sector there, listing in the US would provide great benefits. It would, however, also increase costs by mandating to follow different accounting rules and reporting cycles.

Incorporating Alcon in the US is not an option due to tax considerations. The dual listing would be problematic since the company might not be big enough to sustain liquidity for both markets. ADRs might not attract the right kind of specialized industry investors but rather broad mutual funds.

Considering all these implications, the best option might be to list Alcon in the US but as an officially Swiss company (tax considerations). To make the company appealing to US investors, this strategy would have to be accompanied by making Alcon “look” as American as possible so that analysts and investors can easily “understand” the company.

The minimum IPO price should be the lowest price that values Alcon still higher than it is valued as part of Nestlé (e.g., Nestlé blended EBITDA Multiple applied to Alcon) and covers all costs of the IPO, which is approximately $24 per share. The fair price would be the true equity value of the company when separated from Nestlé, which is $35 per share.

Company and Industry Overview

Is Nestle suffering from a conglomerate discount, and if so, what should be done?

Nestlé is the world’s leading food & beverage company, highly invested in 3 different business units: food & beverages, Ophthalmic, and Cosmetics. The question is now: Does Nestlé trade at a conglomerate discount, and if so, what is the best way to dissolve the issue?

Nestlé’s conglomerate characteristics

Is Nestlé’s value fully appreciated and Alcon’s potential realized?

Conglomerate characteristics of Nestlé

Unrelated Industries

Nestlé is active in a variety of unrelated industries in which the existence and realization of meaningful synergies seem to be unlikely. While Nestlé‘s core industry is food & beverages with a global market share of 1.4%, it also holds…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!