Porsche is a publicly-traded German auto manufacturing firm. Its CEO, Dr. Wiedeking, was the officer in charge since 1993. Analysts are skeptical of speculations on currency movements and that this could affect the company and its stakeholders. Hence, CEO Wiedeking seeks to look back on the strategy of the company when it comes to exposure management.

Michael Moffett and Barbara S. Petitt

Harvard Business Review (TB0119-PDF-ENG)

April 24, 2004

Case questions answered:

- Porsche is a rather special case of corporate governance. Who are Porsche’s primary and secondary stakeholders, and how does current management work with and for those stakeholders?

- How does Porsche differ—operating structure, manufacture, financial results, etc.—from other major European-based auto manufacturers?

- Describe Porsche’s foreign exchange operating (economic) exposure. How has the company been managing this exchange rate exposure? What are the consequences for Porsche if the USD becomes stronger?

- Is Porsche’s currency exposure management strategy significantly different from its major competitors?

- What methods are theoretically available to Porsche to manage or hedge its currency exposure? Why have these other methods not been used?

- How do you think Porsche has been running its currency options hedging program? How are the positions constructed and managed?

a) Assume Porsche had decided to initiate their three-year option hedge program in July 2001.

b) Consider what kind of options Porsche must buy in order to establish its three-year rolling currency option program. When making the calculation and planning, simplify the analysis to an annual purchase and valuation.

c) Employ the Garman-Kohlhagen model to value the options. The ingredients of the model can be found in Appendix 8 of the case.

d) Was Porsche’s strategy profitable when taking option premiums into account?

Not the questions you were looking for? Submit your own questions & get answers.

Porsche Exposed Case Answers

This case solution includes an Excel file with calculations.

Background Information about Porsche

Porsche is a publicly traded German auto manufacturing firm. Its CEO, Dr. Wiedeking, has been the officer in charge since 1993. The company is held by two founding families, Porsche and Piech.

The company has two classes of shares, ordinary and preference, with ordinary shares holding all voting rights. All of the ordinary shares were held by the two families. Preference shares were publicly traded. 50% were owned by large institutions, 36% were owned by small investors, and 14% were again owned by the two families. Its stocks were traded on the Frankfurt Stock Exchange.

From 2002 to 2003, the company garnered €5.582 billion in sales revenue with €565 million in profit.

Porsche was notorious for its stubbornness and refusal regarding disclosure and compliance with reporting standards.

In 2002, the company gave up on listing in NYSE because of the Sarbanes-Oxley Act, using the inconsistency with the German Law as an excuse. The management also refused to report the financial situation quarterly.

Therefore, the company was removed from MDAX. Nevertheless, the company’s attitude was insoluble, saying inclusion in the Morgan Stanley Capital International Index was more critical.

The company also continued to report under German accounting standards rather than US GAAP or IAS, in contrast to its many competitors.

Discussion

The management was compensated, focusing on year-end profitability, with no incentives and stock options. Yet, the management successfully created value for the company’s stakeholders since it managed to increase the share price significantly.

The company continued its operations in different vehicle platforms: the premier luxury sports car, the 911, the competitively priced Boxter Roadster, the off-road sport utility vehicle, and the Cayenne.

Porsche maintained its manufacturing in two countries only, Germany and Finland, whereas its rivals had manufacturing facilities in North and Latin America, the UK, and Europe.

The financial results of the company were remarkable compared to other car producers. Although it had the lowest amount of sales, it had the highest revenue per vehicle, highest EBIT margin, NOPAT margin, ROIC, and P/E Ratio.

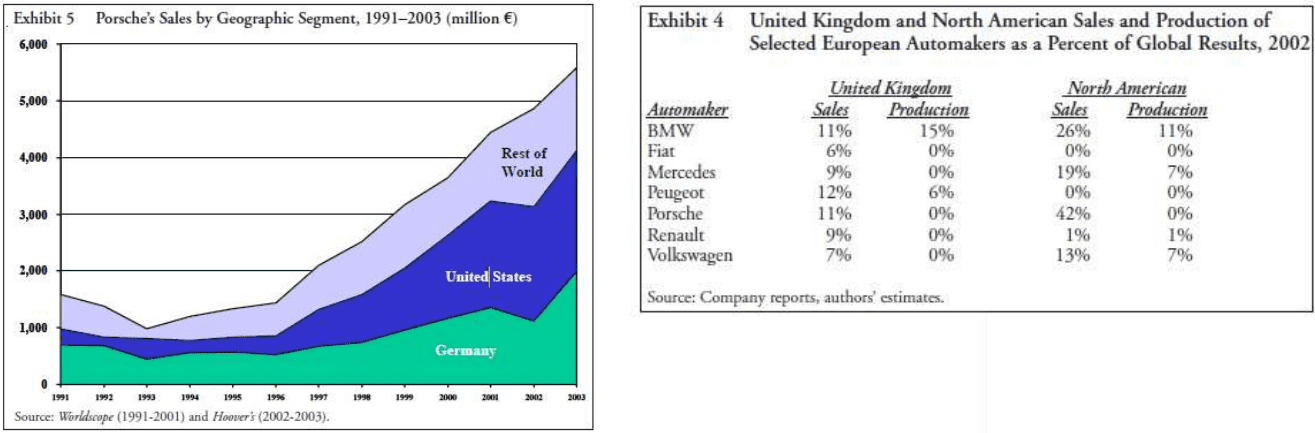

The company’s costs were mainly in euros since its facilities are located in Europe. However, of the company’s revenues, 42% were from North America and 11% from the UK in 2002. Porsche’s non-euro sales were also expected to increase in the future.

Therefore, Porsche was exposed to…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!