This case study focuses on financing the acquisition by RadNet of Radiologix in July 2006. RadNet's acquisition of Radiologix lies in the context of several key factors, which must be considered. Would the financing successfully close the Radiologix acquisition and leave room for long-term growth for RadNet?

Alex Droznik and Susan Chaplinsky

Harvard Business Review (UV6418-PDF-ENG)

August 05, 2011

Case questions answered:

How large should the first tranche of FLD be? For the balance, which would it be: HY debt or SLD? Would the financing successfully close the Radiologix acquisition and leave room for long-term growth for RadNet?

Not the questions you were looking for? Submit your own questions & get answers.

RadNet, Inc.: Financing an Acquisition Case Answers

This case solution includes an Excel file with calculations.

Overview – RadNet, Inc.: Financing an Acquisition

RadNet’s acquisition of Radiologix lies in the context of several key factors.

Geographically, RadNet currently operates solely in California, while Radiologix operates in California, New York, and Maryland. The acquisition will increase the geographic diversification of RadNet and grant access to the east and west coasts of the United States.

Moreover, greater economies of scale will be achieved, given the stronger negotiation stances on the reimbursement rate with commercial payers, enhancing RadNet’s purchasing power.

Thirdly, the integration of the two organizations’ systems and operations will lead to a cost-saving effect by eliminating duplicated expenses and reducing capital expenditure.

Through the acquisition, RadNet will obtain a larger company profile, which yields a stronger credit profile that grants easier access to the capital markets at a lower cost.

To facilitate the acquisition of Radiologix, $362.5 million must be raised through debt financing, preferably. To evaluate the most effective debt financing solution, two models were generated. Future trends of RadNet’s performance were taken from existing due diligence by GE and RadNet (Exhibit 11).

The first model uses the offered debt financing conditions from GE for both the first and second tranche of debt. It is $225.0 million of senior debt, and $137.5 million of privately funded second lien debt (SLD) will proceed.

In this case, both debt tranches have covenants that must be followed. The second case would see senior debt raised to the maximum allowable under the covenants and high-yield (HY) bonds funded through the public market, resulting in a $277.1 million senior debt allocation and a $85.4 million high-yield debt allocation.

Cost of Financing

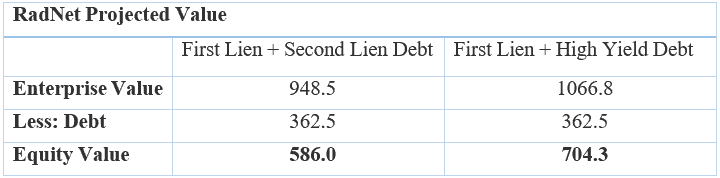

The cost of financing the acquisition of Radiologix will be lower if the HY bond option is taken alongside GE’s senior debt funding. Projecting RadNet’s future performance and cash flows, the company would see a net present equity value of $586.0 million if the debt is financed through SLD.

If financing is achieved through a combination of GE’s senior debt and the HY bond market, a net present equity value of $704.3 million can be realized (Table 1). Hence, from a value perspective, financing through the high-yield bond market is preferred.

Table 1 – RadNet Projected Value

Option One – Private Debt through GE

One debt financing option available is the issuance of additional private debt in the form of SLD with the requirement to maintain an additional set of covenants until maturity. The increased strictness of debt covenants forces RadNet to monitor its performance to prevent the risk of insolvency tightly.

This could lead to declining operational and financial flexibility post-acquisition when the company is adapting to operational adjustments. Although the financial projection of RadNet showcases that the credit metrics are…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!