Restructuring Navigator Gas Transport case study deals with Navigator Gas Transport, a shipping company headquartered in Switzerland and incorporated in the Isle of Man in 1997, which was aspiring at operating semi-refrigerated ethylene-capable gas carriers transporting various cargos around the world. The company, however, ran into difficulties over the course of the shipbuilding phase. The company was unable to meet its contractual liability of interest payments in 2002 and had to eventually file for a petition to reorganize under Chapter 11 in the U.S. Bankruptcy Court. David Butters, Managing Director at Lehman Brothers, is preparing a restructuring plan for Navigator Gas Transport. Butters analyzes if he has sufficient information about, and control over, operations at Navigator to be confident enough to go ahead and pursue lengthy legal proceedings.

C. Fritz Foley

Harvard Business Review (207092-PDF-ENG)

December 18, 2006

Case questions answered:

We have uploaded two case solutions, which both answer the following questions:

- Analyze Navigator Gas’ initial financial policy (capital structure). What may have been the motivation by the founders for setting up Navigator Gas’ capital structure as they did? Would you have bought the First and Second Priority Notes when they were issued in 1997? What was the probability that the interest coverage dropped below 1.00 in the first year? What was the value of the equity at this point in time (assume an asset value volatility of 25%)?

- If you owned the First Priority Notes, would you vote in favor of the plan that Butters proposed, or would you try to negotiate for a different outcome? What if you owned the Second Priority Notes? (In valuing the claims under Butters’ proposed restructuring plan, assume that the free cash flows grow at 2% from 2008 until 2030 and that at the end of 2030, the ships have no value and are scrapped.)

- If Butters had to restructure Navigator under Isle of Man law instead of under U.S. law, would the main differences between these legal systems described in the case have affected the terms of the restructuring? If so, in what way?

- How should Butters respond to Cambridge Gas Transport’s challenge to the ruling by the U.S. Federal Bankruptcy Court?

Not the questions you were looking for? Submit your own questions & get answers.

Restructuring Navigator Gas Transport Plc. Case Answers

This case solution includes an Excel file with calculations.

You will receive access to two case study solutions! The second is not yet visible in the preview.

Executive Summary – Restructuring Navigator Gas Transport Plc. Case Study

Navigator Gas Transport Plc. (hereafter, NGT) filed for bankruptcy, according to Chapter 11 in the United States in the spring of 2004.

Mr. David Butters, Managing Director at Lehman Brothers, has been appointed as chair of the creditor’s committee. His primary responsibility was to construct a prepackaged reorganizational plan that would steadily improve performance if Navigator emerged from Bankruptcy whilst maximizing the creditor’s value.

After filing for bankruptcy, however, creditors became the firm owners, and the equity holders lost all influence and decided to take action. Currently, Butters is experiencing a creditor-favoring reorganization backlash from the equity holders and is being forced to file for bankruptcy in both the Isle of Man and the United States.

Equity holders were not originally content with the creditors’ committee filing in the U.S., and then petitioning under the Isle of Man to extinguish equity is unreasonable as it would be “extra-territorial reach.”

The bankruptcy court of the Southern District of New York accepted the creditor-favoring the pre-packaged plan. However, despite the change of venue, the solution did not appease the equity holders currently “out of the money.”

Now, Butters is facing the Isle of Man’s decision and whether they will go against bankruptcy policy and support the U.S. decision to distinguish equity.

To support Mr. Butters in pursuing the reorganization plan, we will focus on answering the following key problem statements:

1. Start from the very beginning and give an analysis of whether we would have purchased the First and Second Priority Notes when they were issued in 1997 based on NGT’s initial financial policy.

2. Then, we will analyze, according to US bankruptcy law, the approved reorganization plan proposed by Mr. Butters and the creditor’s committee from the perspectives of First Priority Mortgage Notes holders and Second Priority Notes holders individually.

3. We will then address the differences in bankruptcy filing regulations between the United States of America and the Isle of Man and how this pertains to the restructuring of NGT.

4. Finally, address Cambridge Gas Transport’s (hereafter, CGT) challenge to the U.S. ruling and propose several feasible scenarios that Mr. Butters can bring up to answer CGT’s cross-petition.

About Navigator Gas Transport Plc.

The Navigator Gas Transport Plc (NGT) is a shipping company that operates in the charter market. It operates some of the most versatile ships as it can hold special types of cargo. It has a refrigeration system and can be loaded and unloaded with ease. This special cargo includes the entire range of petrochemical gasses, including ethylene, propylene, butadiene, vinyl chloride monomer (VCM), and LPG.

NGT was incorporated in 1997 in the Isle of Man, which is deemed a tax haven, and its headquarters is situated in Lugarno, Switzerland. Due to the nature of the shipping business, NGT conducts business internationally. More specifically, NGT is a company that transports petrochemical gasses and liquefied petroleum gas (LPG). The company was founded in June 1997 and then began making its first investments in ships.

Currently, NGT is undergoing financial distress, and as of the Spring of 2004, it filed for bankruptcy with the request to restructure debt, otherwise known as Chapter 11 in the US. To address the immediate concern of bankruptcy and firm reorganization, NGT must consider several aspects. As was aforementioned, and of utmost priority are the different stakeholders; this includes the manager and how the creditors and equity holders influence them.

Upon filing a Chapter 11, NGT had USD 217 mn. in First Priority Notes and USD 87 mn. in Second Priority Mortgage Notes. The total amount of outstanding debt was, therefore, USD 304 mn. pre-filing. Moreover, NGT had USD 38 mn. outstanding in Equity; its minority shareholders all have a 10% stake in the firm and consist of Arctic Gas, GEBAB, Xenon Shipping, and TGE.

The majority stakeholder of NGT is Cambridge Gas Transport, a company owned by Vela Energy Holdings registered in the Bahamas and has a 60% stake.

I. Assessment of investment in Navigator’s initially issued notes

At first glance, purchasing First or Second Priority Mortgage Notes of Navigator Gas Transport Plc in 1997 may have been an enticing opportunity for several reasons. Typically, however, investing in NGT requires a creditor to bear significant risk.

Whether creditors are willing to bear such a risk depends on the return and the creditor’s individual tolerance to risk. This section will analyze the different risks associated with being a First or Second Priority Note investor.

Furthermore, the analysis will conclude whether NGT undergoes financial distress or economic distress to determine whether NGT is a feasible investment and can survive potential bankruptcy. Therefore, before determining whether it is a good idea to invest, we need to consider all the factors associated with the firm in the case of default or poor performance and whether this is a characteristic of NGT or the industry as a whole.

The initial financial capitalization of NGT involved USD 217 mn. in debt and USD 38 mn. in equity. As their total capitalization is just under USD 335 mn., the proportion debt of total assets is 89%, and the proportion equity, therefore, of total assets is 11%. NGT also pays a high interest rate on its outstanding debts.

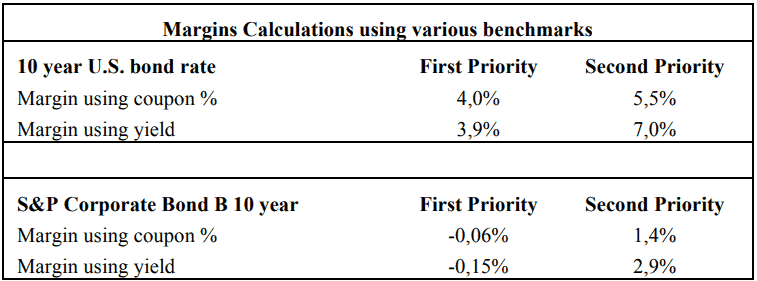

When considering whether to invest in the company upon its inception and initial capitalization, one must note that high-interest rates of 10.5% and 12.0% for the First and Second Priority Mortgage Notes, respectively, do not necessarily mean high returns.

In this case, the shipping industry is renowned for being a risky business, and high interest rates may require in NGT to have strong profit margins to be more risk-bearing. Considering the high outstanding debt in their capital structure relative to equity and the high interest rates on the First Priority and Second Priority Mortgage Notes, the worst-case scenario must be considered when the company defaults and to whom the firm will have obligations.

Having a considerably high debt-to-equity ratio of approximately 7.8 times, the firm may not be able to satisfy an acceptable amount of the creditor’s notes in the case of default.

NGT has a two-year debt repayment pass and does not need to begin repaying interest owed to its creditors until 1999. In 1997, ships are still being made, and only in 1999 are they expected to begin operating. With an 85% utilization rate and its ability to carry specialized petrochemicals, it still may not reach the necessary threshold to pay back interest, let alone the principal.

Despite the financial pressure, NGT will feel in its first years of operation. Arguably, they have a buffer to allow them more time to pay their interest.

NGT’s buffer can issue Second Priority Mortgage Notes for a value of up to USD 20.9 m. In the insolvency zone, NGT would have to use this raised capital to pay its interest payments. Unfortunately, USD 20 mn. is only a fraction of one year’s interest payments.

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!