Sealed Air delved into a program geared towards enhancing manufacturing efficiency and product quality. Less than a year after, it embarked on a loan of the market value of its common stock. The amount borrowed was used as a special dividend to its shareholders. This leveraged capitalization created a disturbance of the status quo and pushed forward internal change. The change included a new objective, changes in the compensation systems and in the manufacturing and capital budgeting system.

Karen H. Wruck, Brian Barry

Harvard Business School (294122-PDF-ENG)

May 10, 1994

Case questions answered:

- Please identify potential leverage deficits.

- Please make a valuation for the recapitalization.

- Make further recommendations for Sealed Air.

Not the questions you were looking for? Submit your own questions & get answers.

Sealed Air Corps Leveraged Recapitalization (A) Case Answers

Purpose and Scope – Sealed Air Corps Leveraged Recapitalization (A) Case Study

This report reviews the outcomes of the financing transaction undertaken by Sealed Air in 1989 and evaluates how much value was created, if any, who benefitted from the recapitalization, what risks the transaction entails, and the trade-offs of the deal.

Executive Summary – Sealed Air

Sealed Air had enjoyed high growth and market share due to strong patents.

As the patents came closer to expiration and with the threat of extreme competition looming ahead, they decided to shift their focus from sales to manufacturing efficiency and value creation. It was clear that a strategic reshaping was soon impending, given that the company was maturing.

Leveraged Recapitalization VS. LBO

As the company had free cash flows in excess of its ongoing needs, it had debt capacity and could create value from interest tax shield gains. Accumulation of cash does not make sense for this company as it is a mature company and has no scope for further innovation.

The company wanted a simple way to return the money to its investors and ruled out the use of unusual financial instruments.

In such a scenario, a leveraged recap is the simplest way to return money to the shareholders whilst simultaneously increasing shareholder value through the capture of tax shield gains and through improved performance resulting from the pressure created by employing debt and having to meet debt service obligations.

Principal repayment of debt every year addresses the problem of cash accumulation. They decided to issue $329.8 million in dividends to shareholders, which accounted for 87% of the total equity.

To pay this dividend, the company recapitalized by issuing debt and, therefore, was faced with high bankruptcy risk, thereby creating pressure to improve operating efficiencies.

Their working capital was too high, and the inventory efficiency was not in an ideal place before employing World Class Manufacturing. The real challenge was to maintain such a good level.

This recap makes sense because employing a large amount of debt would put pressure on both the management and workers, thus improving the performance.

Sealed Air was able to shake up its strategy and restructure its manufacturing because of the restrictions placed on capital spending in the debt covenants, thereby eliminating unnecessary Capex. The recap was successful in helping the company capture tax shield gains and improve its operations.

An LBO could help them get rid of the cash in hand and also vitalize the whole company, but the management could not afford to lose control of the company, which was why they turned to a leveraged recapitalization.

Looking at where we are standing, the leveraged recapitalization did not largely affect anyone but the employees who were under pressure to improve demand forecasting and improve efficiencies to generate positive cash flows to meet debt payments.

The risk of bankruptcy endangers their jobs, while the shareholders do not face such a significant threat as a huge chunk of their investment is already paid out as a dividend. The shareholders took on a relatively smaller risk relative to the potential value creation.

The employees were also given ESOPs, which meant that their income and their investment returns were both tied down by the same risks. However, the company believed that this would make their operations more efficient.

Concerns about the Recapitalization

First, the company’s stock price definitely reveals one of these negative impacts. Before the dividends were paid, the stock price was at $50.75. After the payout, the stock price fell to $12.5. It seemed strange because the stock price should be 50.75-40=10.75$, according to the formula: (Po – Pt) * (1 – Tcg) = Div * (1 – T1).

It is important to note that the tax rate of the dividend was higher than the tax rate of capital gain. This formula told us that, at that point, such a large amount of dividend payment was too expensive.

Second, the company would keep low liquidity for a long time, which means that Sealed Air would be missing out on potential large investment opportunities (Mergers and Acquisitions, for example), resulting in a loss of market shares.

This type of recap would make the company focus on cash flow-generating projects to meet the debt payments. In the worst-case scenario, the company may run into financial distress in a tight market and could even meet with a bankruptcy issue.

Transaction Evaluation

In a successful leverage recap, the value of the dividend plus the value of the stub exceeds the pre-recap share price, which is exactly the case here, as the shareholders were able to do a dividend capture. Sealed Air has done a recapitalization to capture tax shields and increase its shareholder value.

The number of shares outstanding as of April 27th, 1989, was 8.245 million, and the stock was trading at $44.125-$45.875. This puts the unlevered market value before the announcement of the special dividend at $378.24 million (assuming $45.875 share price).

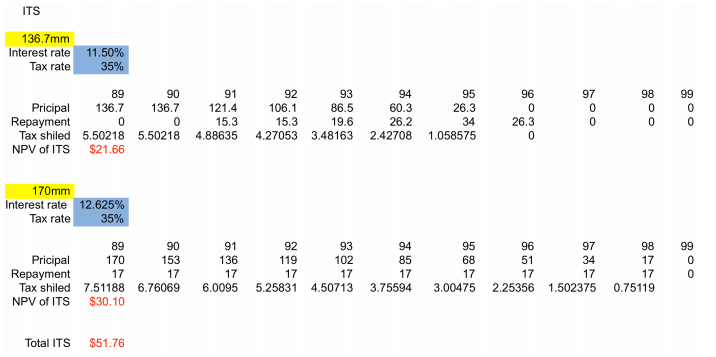

The total debt raised by the firm was $306.7 million, which yielded interest tax shields of $51.76 million (see appendix #1), the value of which can be captured upfront. So the value of the levered firm includes the value of the unlevered firm plus the present value of the interest tax shields, which is $430.72 million ($378.24M+$52.48M).

The value of equity after leverage is the value of the levered firm minus the debt, which equals $124.02 million. The new price of the stock after the debt issue and payout of the special dividend is $15.04 ($124.02M/8.245M).

However, the old price minus the dividend is $5.875, and this does not reflect the value created by the tax shields. The difference in these two prices of pre and post-leverage is the value created by this leveraged recapitalization. The price after the announcement of the levered recap will be closer to the new price calculated ($15.04) as the market prices in the value are created by this financing transaction.

Two days after the announcement, the stub share closed at $12.5. This is still lower than the price of $15.04 we calculated because the market also prices in the probability of bankruptcy and associated bankruptcy costs. Another cost that will also be priced into this new stub share’s value will be the transaction fee of this financing and payout, which is $20.9 million.

The leverage recap was definitely a good idea for Sealed Air because it is optimal to borrow until interest equals EBIT to take full advantage of tax shields as long as the after-tax earnings of debt holders are greater than the after-tax earnings of equity holders. In this case, the company’s level of interest expenses relative to their EBIT was low enough to capture an effective tax advantage of debt.

Conclusions

Overall, the leveraged recapitalization was doing great within Sealed Air. But one thing the management should keep in mind is that once the debt matures, how to maintain the performance.

Companies are like machines, you cannot keep them running 24/7, you have to give it a break. For that, our suggestion is the company should get rid of major parts of its debt and give something to workers and shareholders and then carry on what they have been doing but not raise the leverage ratio to a critical level.

Appendix:

Appendix #1 ITS Calculations

Did this solution help you?

(2 votes, average: 5.00 out of 5)

(2 votes, average: 5.00 out of 5)