Laflin examines a building to be acquired. The property is currently under lease contracts but the said contracts will be expiring soon. He is challenged on whether it is a good property for him to acquire.

Richard E. Crum

Harvard Business Review (390181-PDF-ENG)

April 25, 1990

Case questions answered:

We have uploaded two case study solutions, which both answer the following set of questions:

- Is SouthPark IV a good property for Laflin to acquire?

- What assumptions has Laflin made in creating his setup for SouthPark IV? What changes, if any, would you make to his setup? What is your projected return for the property?

- What price should Laflin offer for SouthPark IV? What conditions should be attached to his offer? How might Lonestar try to justify a higher price? What might SouthPark IV be worth in five years?

- Why are there wide variations in the valuation of real property assets?

Not the questions you were looking for? Submit your own questions & get answers.

SouthPark IV Case Answers

This case solution includes an Excel file with calculations.

We have uploaded two case study solutions. The second is not yet available on the preview.

1. Is SouthPark IV a good property for Laflin to acquire?

First, I would like to consider the economic factors and several quantitative factors to evaluate SouthPark IV.

Economic Factors & NPV

- Since the Houston economy is slowly growing, it is expected to increase demand for space in the near future.

- On the other hand, based on the information provided in the case, almost every category of real estate had a huge supply of vacant spaces. However, from 1986 to 1989, there was no major construction in the area, and the occupancy rate remained at 87%, which shows the high vacancy rate in the area.

- Another major concern regarding the economic factors is the collapse of the savings and loan industry in Texas, which can potentially lead to a decrease in the purchase price as well as rent by flooding the market with highly discounted properties.

- Based on their calculation in Exhibit 4, the NPV is about $1,500,000, with an initial investment of $300,000. However, the NPV calculation should be revisited, and the debt services, as well as tax, should be included in calculating NPV. Considering debt services as well as tax in the calculation, the NPV will end up with a negative value.

Property Assessment

- The building generally is in excellent condition except for the roof, which required to be repaired with an estimated cost of $50,000.

- One of the main advantages of this property is that currently, the building is completely occupied, and the leases were net of common expenses, taxes, and insurance. However, all four leases are going to expire on June 30th, and tenants may not be willing to continue with $2.5 per square foot, and they only agree to stay at the current market base rent of $2 per square foot.

- There are costs associated with turnover, and the NPV should be calculated based on three different scenarios: 1) the current tenants are going to extend their lease for the next 5 years with the current base rent of $2 per square foot; 2) the current tenants are going to extend their lease with their current rent of $2.5 per square foot; and, 3) the current tenants are not extending their lease, so there will be a 5% vacancy rate as well as leasing commission once the tenants are done with the lease.

- The financing terms for SouthPark IV are much lower than the industry and attractive to a potential buyer. This is due to the foreclosure of the property by Lonestar. However, the financing terms are attractive. It is important to note that no one else bid for the property at the foreclosure auction. This factor shows that either the asking price is higher than the true value of the property or this kind of real estate market still is not growing as expected.

Comps

- The deal seems reasonable compared with the recent sales in the area, as can be seen in Exhibit 5 ($1,500,000/80,000 square feet = $18.80 per square foot).

Cash Flow

- According to the financial model presented in the case, over the life of the investment, the investment generates positive cash flow, excluding the initial investment. which implies that additional capital is not required to be raised for future expenses.

Replacement Costs

- Based on the calculation shown in Exhibit 3, the reproduction cost is about $2,037,762, which is significantly higher than the purchase price of SouthPark IV. Comparing the reproduction cost with the purchase price illustrates that it would be cheaper to purchase this property than to build a new one.

Based on Laflin’s assumptions and the above-mentioned factors, the property looks like an appropriate investment. Based on their calculation, the property may not have a high return as it has a positive net operating income.

2. What assumptions has Laflin made in creating his setup for the property? What changes, if any, would you make to his setup? What is your projected return for the property?

Assumptions made by Laflin in his calculations for the investment include:

- Income and expenses will grow at 3%

- Used a 14% discount rate to calculate NPV

- Exit cap rate of 10%

- The price associated with the sale will be 5% of the gross sales price

- Estimation of $50,000 for roof repair

- The tenants would honor their statement that they would extend their leases with their current rent and not the current market price

- 4% management fee

- 5% vacancy

- SouthPark IV will be sold in the 10th year

- Rehabilitation expenses of $15,000

The changes that I would make in his assumptions are:

Laflin had multiple very optimistic assumptions in his setup. That’s why the financials in his calculations look way better than reality. He should count the depreciation cost of the building, which was $38,095 on a 39-year basis, as well as income tax and sales tax.

For the vacancy rate, he should be more conservative in his estimates and use a rate closer to the Houston rental data as well as competitor rental data.

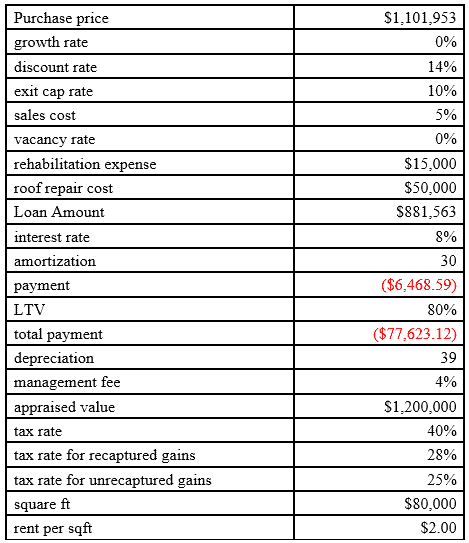

Table 1 lists the assumptions required for the case. The current tenants extend their lease based on the current market rent of $2 per sqft, and there is no growth associated with their rent.

Table 1 List of assumptions for the case of rent based on the market price without any growth

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!