The Timken Company case study discusses significant investment decisions and management of such investments, which may affect a company's financial structure. It allows students to provide the valuation for a firm to determine if it is a good investment or not.

Kenneth Eades and Ali Erarac

Harvard Business Review (UV0519-PDF-ENG)

July 28, 2005

Case questions answered:

- Review the data to identify the relevant cash flows on a forecast basis. Identify the free cash flows. Determine the discount rate appropriate to value the cash flows of Torrington or The Timken Company.

- Attempt a fundamental valuation of Torrington on a standalone basis (i.e., no synergies) valuation.

- How would one perform a multiples valuation of Torrington, and which multiples should be used and why?

- How does Torrington fit with the Timken Company? What are the expected synergies, and what is your synergy valuation of Torrington?

- How do you think Timken should structure the deal – i.e., cash or a stock-for-stock deal? Explain why.

Not the questions you were looking for? Submit your own questions & get answers.

The Timken Company Case Answers

This case solution includes an Excel file with calculations.

1. Review the data to identify the relevant cash flows on a forecast basis. Identify the free cash flows. Determine the discount rate appropriate to value the cash flows of Torrington or The Timken Company.

This report shows the analysis of the acquisition of the target firm, Torrington, by the acquiring firm, The Timken Company. The analysis includes the pre-acquisition valuation of the target, the acquirer, the post-acquisition valuation of the final entity, and the rationale of the acquisition deal.

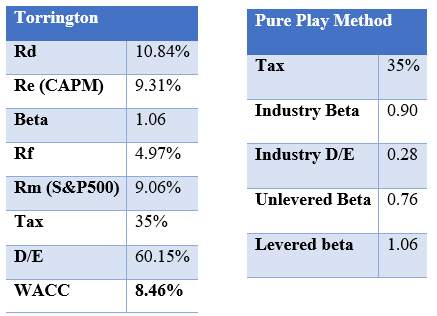

The report starts with the valuation of Torrington. Exhibit 1 shows the inputs to calculate the cost of capital of Torrington:

Exhibit 1: WACC Inputs

To calculate the beta of Torrington, we used the pure-play method rather than just taking the beta of its parent company, Ingersoll-Rand (IR), because the sales of Torrington only take a small part of the total sales of IR, 11.67% and 13.45% in 2001 and 2002 respectively.

Excluding comparable firms that have missing data, the analysis took the average beta value of individual firms in the bearing industry as the levered beta because there is insufficient data to pinpoint specific comparable firms that share the same operation risk as Torrington.

The tax rate used is the federal corporate tax rate of 35%. The industry D/E ratio was obtained from the average of the value of debt over the market capitalization of individual comparable firms.

The D/E of the bearing industry is calculated by summing up all the debt and equity in the market.

After that, the levered beta is calculated from delivering the industry beta and levering it with the tax rate and D/E ratio of IR. For the cost of equity, the CAPM was used.

The expected market return is the average historical return of the S&P 500 over ten years (1993 to 2002), and the risk-free rate used is the long-term government yield because the company is expected to exist perpetually in valuation. The final cost of equity of Torrington is shown in Exhibit 1.

For the D/E ratio, Torrington is assumed to have the same capital structure as its parent company, IR. Thus, the credit rating of Torrington and The Timken Company would be similar.

Using data from the balance sheet and income statement of IR, the credit rating reached for Torrington is B, with an expected yield of 10.84%, according to Exhibit 9. The final cost of debt is recorded in Exhibit 1. The WACC obtained is 8.46%.

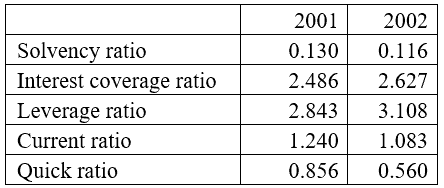

The cost of debt is higher than the cost of equity of the firm. It is an unusual result because of some reasons. Firstly, according to EBITDA/Sales, the firm’s credit rating is B. Thus, the cost of debt is 10.84%. Secondly, solvency and liquidity ratios represent the firm having high credit risk.

The solvency ratio is lower than one, meaning that the Net profit of Torrington is not sufficient to meet a contractual obligation.

Moreover, although the current ratio is greater than one, the quick ratio is lower than one, meaning that the firm is only able to meet short-term debt obligations when it liquidates all current asset items.

The leverage ratio of the firm is also considerably high. The asset is approximately three times higher than equity, reflecting that the firm is heavily relying on debt.

In short, it signals that the firm has a considerable credit risk.

Assumptions for Balance Sheet and Income Statement

- Due to the lack of financial data on Torrington, IR’s financial statement is used to forecast Torrington’s financial statement from 2002 to 2007.

- The interest expense for the respective year depends on the outstanding amount of short-term and long-term debt for that particular year. The assumed interest rate and tax rate are 11.5%, which is the interest expense over the total debt in 2002 and 35%, respectively. The tax rate used is the US federal tax rate on corporations.

- The portion of each line item on IR’s balance sheet to IR’s sales is constant for Torrington’s balance sheet throughout the forecasting period. For example, the percentage of IR’s cash over IR’s sales is 3.82%. Consequently, the amount of Torrington’s cash will be 3.82% x Torrington’s sales. For more detail, see the exhibit (xx).

- The net property, plant, and equipment (NPPEt) account of Torrington is calculated by adding capex and subtracting depreciation to NPPEt-1. The amount to balance the accounts will be added to shareholders’ equity.

2. Attempt a fundamental valuation of Torrington on a standalone basis (i.e., no synergies) the valuation.

Exhibit 2: FCFF and Valuation of Torrington

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!