Voyages Soleil (VS) was a tour operator settled in Quebec. Due to the concern of Canadian dollar depreciation, Jacques Dupuis, the president, and owner of VS, considered hedging Canadian dollars.

Stephen Sapp; Jonathan Michel

Harvard Business Review (905N24-PDF-ENG)

October 04, 2009

Case questions answered:

- What option should Voyages Soleil take?

a.) Alternative 1 – Do Nothing

b.) Alternative 2 – Hedge via a forward contract

c.) Alternative 3 – Borrow CAD to invest in USD

Not the questions you were looking for? Submit your own questions & get answers.

Voyages Soleil: The Hedging Decision Case Answers

EXECUTIVE SUMMARY

Voyages Soleil (VS) was a tour operator settled in Quebec. The company usually booked the stays for its customers in U.S. dollars and received payments in Canadian dollars. After the 9/11 event in 2001, the Canadian dollar had depreciated against dollars, and the company had booked payables for 60 million Canadian dollars. Therefore, the firm needed to consider whether to enter hedging activities.

There are four factors that impact currency value, namely, inflation rate, interest rate, the term of trade, and capital flow. Interest rate and capital flow affect currency in the short term (6 months), while others affect the currency in the long term (1 year). After analyzing the indicators, the Canadian dollar would be depreciated in both the short and long term.

As for hedging, VS should buy a forward contract because hedging would reduce currency risk and generate a positive NPV for the firm. Apart from a forward contract, there are also alternative ways to hedge, for example, currency matching and leading and lagging.

However, the decision over hedging activities needs to be considered carefully. There are other determinants that firms should take into account, such as their capital structure, risk profile, opportunity cost, and the prediction of future economic activities.

VOYAGES SOLEIL’S PROBLEM

Voyages Soleil (VS) was a tour operator settled in Quebec. The company has sold travel packages to its customers for a long period of time. The packages included travel tickets and hotel rooms at any desired destination. The company usually booked aboard stays for its customers in U.S. dollars. On the other hand, it received payments from its customers in Canadian dollars.

Obviously, the firm was exposed to exchange rate risk. If the value of the U.S. dollar increased, it would benefit the firm. Unfortunately, even though Canada’s economy was strong, the post-9/11 event influenced Canadian dollars to be weakened against U.S. dollars.

Due to the concern of Canadian dollar depreciation, Jacques Dupuis, the president and owner of VS, considered hedging Canadian dollars. The number of hotel payables was $60 million.

FACTORS THAT IMPACT CURRENCY AND HOW THEY AFFECT A CHANGE IN EXCHANGE RATE

As Dupuis was thinking about hedging, he should have analyzed all the factors that impacted currency fluctuations. The factors are as follows:

1. Inflation rate

Inflation indicates the change in the exchange rate in the long run. The inflation rate changes inversely against the value of the nation’s currency. For instance, if one nation has a negative inflation rate, the value of its currency will be stronger in the long term. According to the case study, Canada’s inflation rate was higher than the U.S. inflation rate1 [See Exhibit 3]

This would result in the depreciation of Canadian dollars against U.S. dollars in the future.

2. Interest rate

Generally, in the short term, a higher interest rate attracts foreign investment to one nation. It consequently leads to an increase in demand for the nation’s currency, which brings about a rise in the nation’s currency value. Conversely, the lower interest rate tends to be unattractive for foreign investment and accordingly decreases the currency value.

However, according to IFE theory, in the long run, an interest increase causes a permanent increase in the country’s money supply. This brings about a proportional long-run depreciation of the currency.

In this case, the Canadian interest rate was higher than the U.S. interest rate at this point in time. Thus, in the long run, the higher interest rate would lead to the depreciation of Canadian dollars. This resulted from a rise in the interest rate that enhanced demand for Canadian dollars in the short run.

Nevertheless, in the long term, the increase in interest rates led to a situation where people could borrow less. By borrowing less, it means they could spend less, which slowed down the economy. It would impact a decrease in inflation, and in the end, in the long term, the value of Canadian dollars would depreciate.

3. Term of trade

The term of trade is relevant to a nation’s GDP. According to the case study, Canada’s GDP had been expanding. This would result in the rise of the nation’s imports and an increase in demand for foreign currencies, which would cause Canadian dollars to depreciate.

4. Capital Flow

Capital flow is relevant to GDP. Canada’s GDP had been rising continuously, which attracted capital inflows that exceeded capital outflows. Therefore, this would lead to an appreciation in Canadian dollars.

All in all, in the short-run (6-month length), the exchange rate is affected by two factors, which are the interest rate and capital flow. However, in this case, the Canadian interest rate was higher than the U.S. interest rate. Accompanied by Canada’s GDP, which was higher than the U.S. GDP, capital would flow into Canada. It would consequently generate an increase in demand for Canadian dollars.

Therefore, Canadian dollars would strengthen U.S. dollars suddenly. However, over a period of time, after foreign investors received the desired amount of returns, they would later leave the investment in Canada. This would, in the end, bring about the depreciation of the Canadian dollar value in six months.

On the other hand, in the long run (one-year length), the exchange rate is impacted by inflation and the term of trade. Since Canada’s GDP is inclined to enhance continually, it would lead to an expansion in Canada’s imports and a rise in Canada’s inflation compared to foreign countries. The larger imports and the higher inflation resulted in the need for foreign currencies and would bring about the depreciation of Canadian dollars in the long run.

THREE DECISIONS FOR VOYAGE

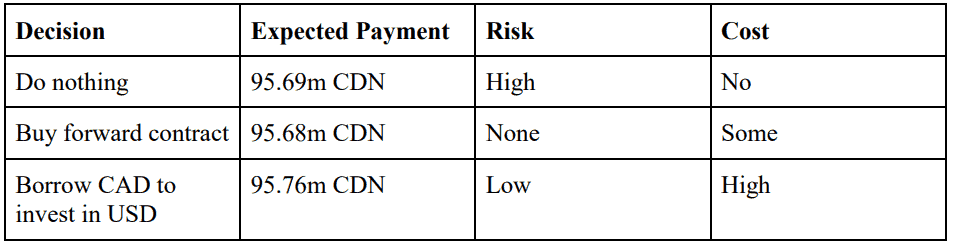

Option 1: Do nothing (Buy at future spot price)

As option 1 is the fact that VS would wait and exchange Canadian dollars in October at the prevailing spot rate at that time, we can categorize the possible outcomes in October into 3 cases:

- No change in spot rate: VS would need to pay 95.27 million CDN (rate = 0.6298) for their booking payables.

- CDN Depreciates: VS would apparently need more than 95.27 million CDN for their booking payables.

- CDN Appreciates: VS would, fortunately, pay less than 95.27 million CDN for their booking payables.

However, we apply the International Fisher Effect (IFE) theory to estimate the expected exchange rate of U.S. dollars against Canadian dollars. It turns out that, according to our calculation, the projected rate is 0.6270 US/CDN. This means that VS should pay 95.69 million CDN for their booking payables.

Option 2: Buy a forward contract

Option 2 states that VS agreed to buy a forward contract at the rate of 0.6271 US/Cdn in April. Consequently, the total amount VS would agree to pay was 95.68 million CDN (60 million USD). The contract must be made in April, and VS needed to find a counterparty who would agree to deliver 60 million U.S. dollars in October. Nonetheless, there are disadvantages to a forward contract.

First, it is hard to find a counterparty that can fit in. Both parties need to match in terms of the demanding amount of money and time maturity.

Second, there exists a counterparty risk for a forward contract. There is a possibility that one counterparty will not deliver the underlying asset. However, these drawbacks are hard to be valued in number. The benefits of a forward are that it hedges the firm against the exchange rate risk.

As Dupuis is concerned about transaction exposure the most, a forward contract was a good option for him to reduce the firm’s sensitivity towards exchange rate volatility.

Option 3: Borrow Canadian dollars to invest US dollars

Option 3 claims that VS decided to borrow 94.49 million CDN from a bank at the annualized six-month interest rate of 2.70%. Afterward, VS would exchange the borrowed Canadian dollars with U.S. dollars at the current rate of 0.6298 USD/CDN. Then, the firm would invest those amounts of U.S. dollars in the USA at the annualized six-month interest rate of 1.65%.

Therefore, when the booking payables are due in October, VS would have 60 million U.S. dollars stemming from borrowing and return on investment. This amount of U.S. dollars could be translated into 95.76 million CDN in October.

VOYAGES SOLEIL’S DECISION

Among these three options, it would be best for VS to…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!