Two Warburg Pincus partners are trying to decide whether to take a portfolio company public and on what stock exchange. The company, Norway-based ElectroMagnetic GeoServices (emgs), has developed a market-leading technology that determines whether an undersea rock formation contains oil - prior to the oil company drilling a hole. The partners need to decide what to do before the IPO window for energy-related companies closes.

G. Felda Hardymon; Ann Leamon

Harvard Business Review (807092-PDF-ENG)

May 29, 2007

Case questions answered:

Case study questions answered in the first solution:

- I need to know at what valuation EMGS could go public. Apparently, the owners are not sure whether to pitch EMGS as a tech OR an energy firm, so the idea is that we cover both angles and value the firm for both alternatives. The firm’s advisors have come forward with some suggestions on how to pitch things – table 10 has the data. Assume that the betas we are given are unlevered. Start out by considering EMGS as all‐equity financed.

a) I need free cash flow figures. Also, how do we get investments? We need to figure that out somehow, given what we have.

b) Value the firm using the info about the high‐tech firms that we have been given. Which comparisons would you recommend to use? - Value the firm as an Energy/Oil firm. How should we position EMGS within the energy industry? Should we decide by looking at the comparable metrics, or would you recommend some other method?

- How much underpricing do we need to take into account? I have some good arguments on what to expect, i.e., 5, 10 or 15%. Assume that the average both in the US and Norway has been around 10% in recent years.

- How many new shares do EMGS need to sell? And how many shares would Warburg need to sell to generate at least a 25% free float?

- Does it make sense to repay the mezzanine bond immediately? What would be the value of the tax shield if these guys stick to this bond indefinitely?

- Also, have a brief look at this competitor (OHM) and tell me if there is anything to be learned, given the info that we have, or is this info just rubbish? More importantly, discuss how we can set EMGS apart from OHM.

- Where should EMGS go public? I have a hunch that the owners prefer NY, but I think that Oslo will be a better fit, so please analyze both options to make sure that we have done our homework. Provide me with a detailed discussion of the advantages and disadvantages of both alternatives and then highlight the three most important arguments for each location.

- As we need to come up with one final strategy, what angle do you think is the one to be more likely to succeed? And which angle would likely result in a higher valuation? Where should they go public? Provide me with a brief summary and a recommendation on how I should pitch things tomorrow.

Case study questions answered in the second solution:

- Valuation

- Offshore Hydrocarbon Mapping (OHM)

- Where to go public?

- Executive summary

Not the questions you were looking for? Submit your own questions & get answers.

Warburg Pincus and emgs: The IPO Decision (A) Case Answers

This case solution includes an Excel file with calculations.

You will receive access to two case study solutions! The second is not yet visible in the preview.

Executive Summary – Warburg Pincus and emgs: The IPO Decision (A) Case Study

The purpose of this document is to discuss the overall strategy for the upcoming Initial Public Offering of Electromagnetic Geoservices AS (EMGS), a Norwegian company with an innovative seabed logging (SBL) technology used for oil and gas exploration. The owners want to go public to take advantage of the open IPO window to secure cheaper funding for the firm’s steep growth curve and to increase liquidity for all shareholders.

The projected cash flow for the future years suggests that the inflows would only start from 2010 as the firm would be heavily invested in working capital in the coming years. EMGS could be positioned as a technology firm or as an energy services company. The valuation of the firm would differ in both instances due to the differences in comparable companies of that specific industry. In the technology industry, there is only one reasonable comparable firm (tomtom), while in the energy sector, the positioning of EMGS would be in a general oilfield service industry.

The value of the firm as a technology company would be $1.39 billion, whereas the value of the firm as an energy services company would be $1.05 billion. As there would be underpricing, EMGS would not be able to attain the full value of the firm, and therefore, the value of the firm under an IPO would be less than its intrinsic value.

The discount value has been assumed to be 10%. Therefore, the IPO value for EMGS would be $984 million if listed under the energy sector or $1.25 billion if the management decides to list it as a technology firm.

The company had taken up debt in the form of a Mezzanine bond, and the benefits of the tax shield of the debt have also been looked into to recommend the appropriate method of bond treatment. It is suggested that the firm does not pay the bond immediately.

The firm can afford to keep debt on its books for a long time as the firm has a bond debt of only $19 million. The value of the firm would increase by $6 million if the bond is kept till perpetuity.

The report also looks into the ex-ante underpricing values for the exchanges in question for the IPO (Oslo and New York). In the Oslo Stock Exchange, the average underpricing for the tech and energy firms is less than 5%, whereas in the U.S., it is approximately 16% around 2006-2007. Also, the failure rate of Energy and Tech firms in Oslo is considerably low. Considering the quality of management EMGS has, we expect the underpricing to be less than 5% on the Oslo Stock Exchange and/or around 16% or higher at the NYSE.

EMGS only pure-play SBL competitor, Offshore Hydrocarbon Mapping (OMH), recently went public with a valuation of $87.4 million and was often held up as an example of the type of performance and valuation to be expected for EMGS.

Taking a closer look, however, reveals the clear differences between the two. We propose that the multiples that can be derived from their IPO valuation be used as the lowest range for EMGS IPO valuation.

The report finally proposes that EMGS be listed on the Oslo Stock Exchange. It is based mainly due to management’s opinion about what they are comfortable with and by avoiding the initial and annual costs of listing on the New York Stock Exchange.

The main concerns about listing in Oslo stem from its market size and heavy exposure to Oil and Gas, which could, in some scenarios, pose a threat to liquidity. We feel that the benefits of listing in Oslo outweigh the potential liquidity gains from New York.

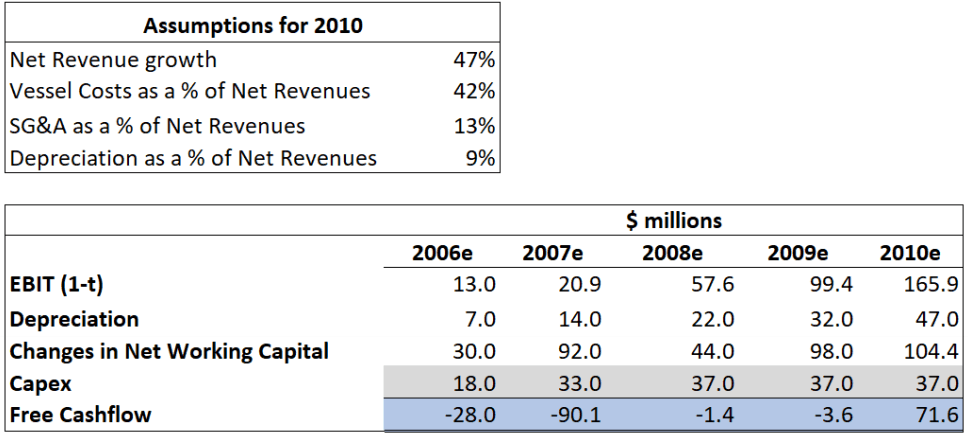

Free Cash Flows

The firm is valued using its free cash flows. The projected financial statements provided have been used as the base for the valuation. Tax rates in Norway are 28%, which is used to calculate the after-tax Earnings before Interest.

Depreciation is added to it while the changes in net working capital and capital expenditures are deducted to arrive at the free cash flows. The capital expenditures are calculated using the following method:

Non-current assets in the current year – Non-current assets in the previous year + Depreciation charged in the current year

This method was used as the values of investment were not stated directly in the projected financial statements. The free cash flows for the years 2006-2009 are negative as the company is investing a lot in the operations of the firm, and therefore, these negative values cannot be used as valuation parameters.

Therefore, the cash flow analysis is extended to 2010 by calculating the cost ratio as a percentage of net revenues of 2009 and using those assumptions to calculate the free cash flow for 2010. The net revenues increased by 47% in 2009, and the same ratio was used to increase the revenues for 2010 (Appendix I).

Appendix I – Free Cash Flows

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!