The Warren E. Buffett, 1995 (v. 1.7) case study deals with the bid price offered by Berkshire Hathaway's for GEICO Corporation. The point to be noted is that Geico's stock price was 55.75% before the acquisition announcement. The price for the acquisition was $70, and about $34.25 million worth of shares were already in the firm of Warren Buffett.

Robert F. Bruner

Harvard Business Review (UV0006-PDF-ENG)

October 11, 1996

Case questions answered:

- Warren Buffett of Berkshire Hathaway is taking the acquisition of the company Geico. Highlight the market’s reaction.

- Determining under/over-valuation using the IRR method compared with opportunity cost.

- Use Value Line Information to Assess Geico’s Stock Valuation Based on Intrinsic Value

- Use Value Line Information to Assess Geico’s Stock Valuation Based on Future IRR

a)Annual IRR for each of high and low ends of range with the beginning price at $55.75

b)Based on the estimated future IRR, was Geico adequately considered undervalued before the acquisition? - Determine the intrinsic value instead of using the Value Line’s forecasts using pure two-stage DDM.

- Determining over-/under-valuation via using the pure two-stage Dividend Discount Model to assess whether Geico stock was undervalued before the announcement was made.

- Determine the over/undervaluation via the back-of-envelope method to the expected return.

- Describe in detail Warren Buffett’s Investment Philosophy.

- Calculate Geico’s ROIC.

- Elaborate on Geico’s potential competitive advantage and cost-efficiency.

- Explain the investment philosophy for investing in a perfectly efficient market.

- Explain the Investment Philosophy for Investment Decisions in the Imperfectly Efficient market.

Not the questions you were looking for? Submit your own questions & get answers.

Warren E. Buffett, 1995 (v. 1.7) Case Answers

This case solution includes an Excel file with calculations.

1) Warren Buffett of Berkshire Hathaway is taking the acquisition of the company Geico. Highlight the market’s reaction.

The point to be noted is that Geico’s stock price was 55.75% before the acquisition announcement. The price for the acquisition was $70, and about $34.25 million worth of shares were already in the firm of Warren Buffett.

But this time, through acquisition, Geico will become an integral part of Berkshire Hathaway. The market value of Geico’s outstanding shares, worth about $67.9, will be added to the market value of Berkshire Hathaway.

It’s shown on page 1 of the case that Berkshire Hathaway’s market value went up by $718 when the announcement was made to acquire Geico.

Calculating the Intrinsic value of Geico’s stock:

718,000,000=34,250,000*(70-55.75) + 67,900,000*(P-70)

=488,100,000+67,900,000P-4753000000

67,900,000P=718,000,000-488,100,000+4753000000

P=4982900000/67,900,000

=$73.39 million is the intrinsic value

It evidently seems that the market views the acquisition of Geico to be over-priced. Still, this acquisition generated interest in Warren Buffet and having acquired it for his firm Berkshire Hathaway. The acquisition resulted in an increase in the stock price of Berkshire Hathaway by 2.4% and increased the market value by $718 M.

When the intrinsic value is calculated, which turns out to be $73.39 million, and when compared to the stock price before the acquisition announcement, which was $55.75, it is clear that the intrinsic value is greater than the bid price.

For this reason, the stock is considered to be undervalued, which is what Warren Buffett prefers to seek: undervalued stocks that have the potential to rise in the future.

Additionally, the intrinsic value was calculated to be $73.39, and the acquisition price was stated to be $70. In this case, the intrinsic value is greater than the acquisition price by $3.39. From this point of view, we conclude that the actual price paid for acquiring Geico’s stock was at a discount.

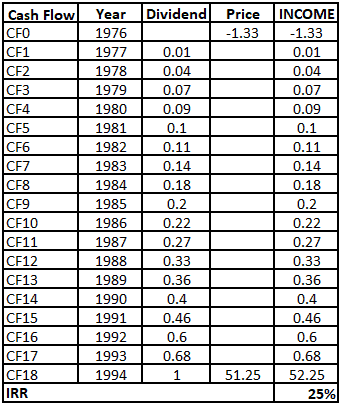

2) Determining under/over-valuation using the IRR method compared with opportunity cost.

As stated in the case, Berkshire Hathaway began purchasing in Geico in 1976 and accumulated a 33% interest by 1980; that is 34.25 million for 45.7 million.

Calculating Price Per Share = 45.7/34.25 = $1.33 per share. Since it’s not given in the case, assume that the year-end market price was 51.25 for Geico in 1994.

Now Calculating Capital yield. The number of years between 1994 and 1976 is 18 years.

= (51.25/1.334)^(1/18) -1=22.47%

Dividend Yield= IRR-CGY= 25%-22.47%

Dividend Yield=2.53%

The 25% IRR was calculated as compared to Geico’s return-on-equity of 11%. As stated in the case, it’s clear that the stock was undervalued because the return on equity stated is more than half of the IRR calculated. This strongly implies that Geico’s stock was undervalued.

Additionally, the 25% IRR is greater than the opportunity cost of…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!