"Yale University Investments Office: August 2006" case study focuses on the dilemma of the investment office to make a decision on the future allocation of the fund to various asset classes that they were investing in to make sure they maximize their Sharpe ratio over the long term.

Josh Lerner

Harvard Business Review (807073-PDF-ENG)

January 03, 2007

Case questions answered:

- What allocation policy should Yale follow?

- How illiquid should the portfolio be?

- How important should proper benchmarks be?

Not the questions you were looking for? Submit your own questions & get answers.

Yale University Investments Office: August 2006 Case Answers

Executive Summary – Yale University Investments Office

Yale’s endowment fund came into existence in the year 1818 and grew to $5 million by the end of its first century. David Swensen, a former Ph.D. from Yale in Economics, was hired to head the Yale University Investments Office in 1985. Under his management, the endowment fund has grown from $1 billion to $18 billion and outperformed its peers.

The primary reason for Yale’s superior long-term performance seems to be its distinctive investment philosophy and the excess returns generated by the portfolio’s active managers. Their philosophy revolves around having a large portion of the fund allocated to equities, diversification, and seeking opportunities in less efficient markets.

The endowment relies on external managers with advanced knowledge and track records in their own segment. Yale focuses critically on the explicit and implicit incentives facing outside managers, trying to structure innovative relationships and fee structures to better align interests.

The investment office has to make a decision on the future allocation of the fund to various asset classes that they were investing in to make sure they maximize their Sharpe ratio over the long term. They should also take into account sufficient liquidity to cover their operating commitments.

The Investment Office has rising concerns about the increasing level of illiquidity in their portfolio. The illiquidity preference, however, might have been a huge factor in their ability to generate excess returns. By selecting superior managers in nonpublic markets characterized by incomplete information and illiquidity, they can seek higher alphas.

We advise that the endowment maintain a portfolio liquidity ratio of one-third in order to avoid forced liquidation below fair value in case of a financial market collapse.

Another rising concern is the lack of proper benchmarks for the portfolio’s assets and managers. The benchmarks are used as an important tool in gauging the performance of any investment in any asset class.

In Yale’s case, proper benchmarks were essential for evaluating the external manager’s performance and creating appropriate fee structures. However, these benchmarks do not really give an indication of the level of risk undertaken or the volatility of return achieved.

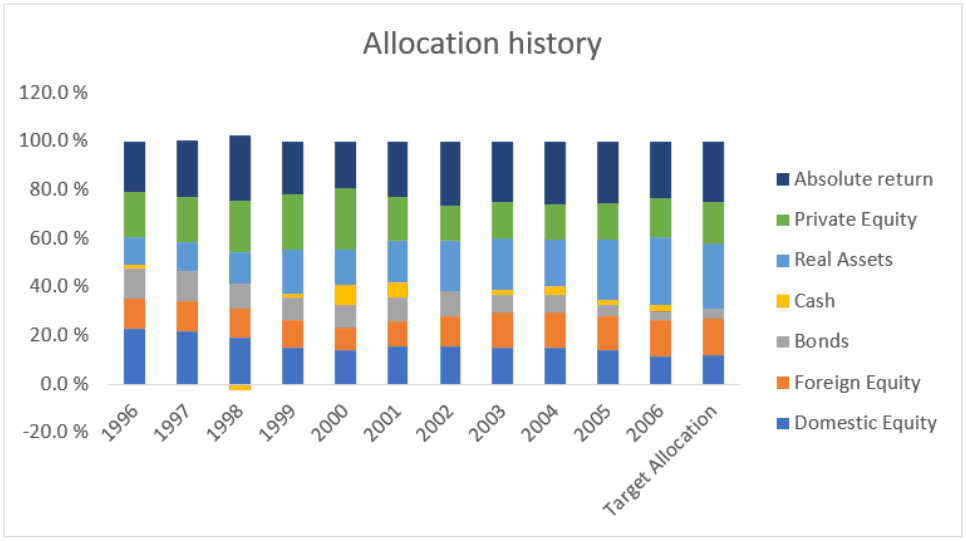

Allocation Policy

Private Equity was one of the most important asset classes for Yale, and this, combined with real assets, made their endowment fund stand out from the rest of the peers.

They started investing in private equity in the early 1970s and increased the proportion they invested until recently, when the target allocation was decreased to 17%.

They focused more on buyouts and hedged their excess positions, which allowed them to make new commitments as they felt that the option to enter again would be minimal if they decided to exit.

They also moved to international private equity markets as the competition in the U.S. strengthened, and there were fewer opportunities available.

The real assets portfolio had a 27% target allocation and was subdivided into real estate, oil & gas, and timberland. It was uncorrelated with the equity market and therefore diversified their risk.

All these tactics paid off handsomely as the total return in 2016 was 22.9% on the whole fund, while the annualized return for the past two decades was 15.4%, surpassing all benchmarks and outperforming peers.

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- You'll be redirected to the full case solution.

- You will receive an access link to the solution via email.

Best decision to get my homework done faster!

Michael

MBA student, Boston

Best decision to get my homework done faster!

Best decision to get my homework done faster!